Understanding the Capital Stack in Real Estate Investing

Financing a real estate deal can be complex. Investors must manage tight deadlines, competing priorities, and stakeholders who depend on their ability to close transactions efficiently. Adding to the challenge is the variety of financing sources available, each with distinct requirements. These funding sources collectively form the capital stack, or cap stack. This is a crucial concept in real estate that dictates how debt investments and equity financing are layered in multifamily real estate and commercial real estate deals, impacting risk, returns, and payment priority.Capital Stack Definition:

What Is A Capital Stack in Real Estate?

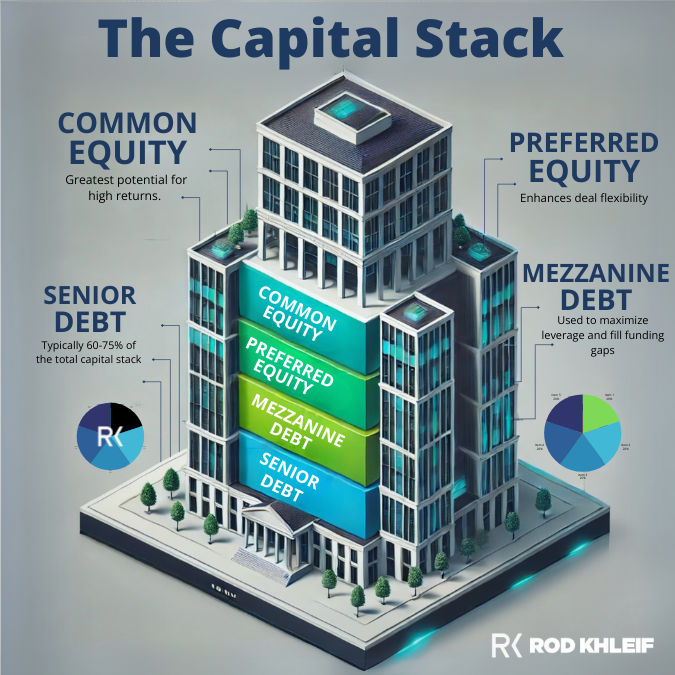

A capital stack refers to the structured layers of financing used to fund a real estate investment, outlining the priority of debt and equity claims on cash flow and profits. It typically includes senior debt, mezzanine debt, preferred equity, and common equity, each carrying different levels of risk and return. It shows the order of claims to cash flow and profits from the property. This applies during the investment period and when sold. Understanding the meaning is essential for assessing risk and potential returns in commercial properties capital stack structures. Most real estate transactions have four primary components of the cap stack, each with a different level of risk and return:- Senior Debt

- Mezzanine Debt

- Preferred Equity

- Common Equity

Senior Debt: The Foundation of the Capital Stack

Senior debt is often the largest part of the commercial real estate loan structure and top of the capital structure, typically covering 65% to 75% of a property’s purchase price. This portion of the real estate stack is the least risky for lenders and investors, as it holds the first lien position on the property. Key features of senior debt:- First in line in payment priority through periodic debt service payments

- Secured by the property as collateral

- Lower interest rates due to minimal risk

- Can initiate foreclosure

Mezzanine Debt: Filling the Capital Gap

In some cases, a capital stacking loan may be required to bridge the difference between the maximum supportable loan amount and the total financing needed for a transaction. This is where mezzanine debt comes into play, offering a flexible funding solution that sits between senior debt and equity financing in the capital stack.

Mezzanine debt is:

- Not secured by the property itself but by a pledge of the ownership interest

- Second in line for repayment, following senior debt

- Associated with higher interest rates to compensate for increased risk

- Often used when equity funding falls short, helping sponsors complete financing for a deal

Mezzanine lenders play a crucial role in structuring real estate transactions, providing capital that allows investors to acquire or develop properties with less equity. However, because mezzanine debt holders are subordinate to senior lenders, they take on greater risk in exchange for higher potential returns. While they may have certain foreclosure rights, their ability to recover capital depends on the property’s financial performance and market conditions.

When structured correctly, mezzanine financing allows investors to maximize leverage while keeping control of their equity, making it an essential tool for scaling in multifamily and commercial real estate.

Preferred Equity: Mid-Level Risk and Reward

Unlike debt, preferred equity represents an investment in the ownership entity rather than a loan. Investors in preferred equity receive:- A priority return before common equity holders

- Higher yields than mezzanine or senior debt

- Profit participation upon property sale (if available)

Common Equity: Highest Risk, Highest Reward Position

At the base of the capital stack, common equity investors assume the highest risk but also stand to gain the most if the project is successful.

Common equity investors:

At the base of the capital stack, common equity investors assume the highest risk but also stand to gain the most if the project is successful.

Common equity investors:

- Have an ownership stake in the property

- Are last in line for repayment if there’s default

- Require higher returns due to increased risk

- Benefit the most from a profitable sale

Why is common equity considered the most attractive position for investors?

Common equity is where the true wealth-building happens in multifamily real estate. These commercial real estate investors:

- Own a piece of the property, benefiting from cash flow and appreciation.

- Receive tax advantages like depreciation deductions.

- Have unlimited earning potential compared to fixed-return investments.

- Get paid last, but in a strong deal, this means enjoying the largest profit share.

The key to success? Investing in well-structured deals with experienced sponsors who know how to maximize value.

The Capital Stack in Action: A Bankruptcy Example

A properly structured commercial investment stack ensures each layer of financing has a designated claim on cash flow and assets. To understand how this works, consider the following capital stack real estate scenario: An investor acquires a multifamily real estate property for $3 million and secures the following financing:- $1.8 million in senior debt

- $200,000 in mezzanine debt

- $200,000 in preferred equity

- $800,000 in common equity

- Senior debt holder is repaid first, receiving $1.8 million.

- Mezzanine debt holder claims the remaining $200,000.

- Preferred equity and common equity holders lose their entire investment.

Why the Capital Stack Matters in Multifamily Real Estate

For investors involved in multifamily real estate, analyzing the cap stack is crucial to structuring profitable deals. Key considerations include:- Risk vs. reward assessment based on financing position

- Return expectations for debt vs. equity investments

- Cash flow priorities in different capital stack structures

How do sponsors structure the capital stack?

Most deals are structured to maximize returns while managing risk. A typical multifamily real estate deal might look like this:

- 70-80% Senior Debt (Bank loan)

- 5-10% Mezzanine Debt (If used)

- 5-15% Preferred Equity (Institutional or private investors)

- 10-30% Common Equity (Investors & general partners)

The common equity group reaps the biggest rewards when the property performs well.

How does leverage affect the cap stack?

Leverage, or using debt to finance a deal, plays a crucial role in shaping the capital stack in a commercial real estate loan. By incorporating debt, sponsors can reduce the amount of equity needed, which in turn increases potential returns for investors. A well structured deal with smart leverage allows investors to put less money into a project while still benefiting from property appreciation and cash flow.

That said, leverage is a double-edged sword. Too much debt can strain cash flow, create refinancing challenges, and put equity investors at greater risk if the market shifts. The key is balance. So, investors should carefully assess loan-to-value ratios, debt service coverage, and long-term financing options to ensure stability.

When used wisely, leverage can help investors scale their portfolios faster and maximize returns while keeping risk in check.

Final Thoughts on the Capital Stack from Rod Khleif

Mastering the capital stack is one of the most important skills you can develop as a multifamily investor. Why? Because how a deal is structured determines who gets paid first, who carries the most risk, and ultimately, how much profit each investor can expect. If you don’t understand where you sit in the capital stack, you’re flying blind. And that’s how investors lose money.

The key to successful investing is striking the right balance between risk and reward. Senior debt may offer security, but it won’t create life changing wealth. Common equity offers the biggest upside, but it comes with the highest risk. Smart investors learn how to analyze each layer of the capital stack, ask the right questions, and structure deals that protect their downside while maximizing returns.

I’ve seen investors create incredible wealth by using the right mix of debt and equity at the right time. But I’ve also seen investors wipe out their portfolios because they didn’t fully understand the risks of over-leverage or poorly structured financing. The difference between success and failure in this business comes down to education and execution.

So, whether you’re raising capital, investing passively, or structuring your own deals, make sure you understand every layer of the cap stack. The better your grasp of financing, the better positioned you’ll be to grow your portfolio, protect your investments, and build a lifetime of cash flow.

If you’re serious about scaling your multifamily business, join me at my next Multifamily Bootcamp. We explore real estate financing, capital stack strategies, and deal structuring. This helps you make better investment choices. Let’s take your investing to the next level!

Capital Stack FAQ

What is a capital stack in real estate?

The capital stack refers to the layers of financing used to fund a real estate deal. It outlines who gets paid first, the level of risk each participant takes, and how returns are distributed among lenders and investors.

What are the main components of a capital stack?

The four primary components are senior debt, mezzanine debt, preferred equity, and common equity. Each layer has different risk and return expectations.

Why is the capital stack important for investors?

It determines priority of payment, level of risk, and potential returns. Understanding the capital stack helps investors evaluate the security of their investment and predict their cash flow.

What is senior debt in a capital stack?

Senior debt is the first layer of financing and has the highest repayment priority. It usually comes from banks or institutional lenders, carries the lowest risk, and offers the lowest return compared to other layers.

What is mezzanine debt?

Mezzanine debt sits between senior debt and equity in the capital stack. It carries higher risk than senior debt but offers higher returns. Lenders often secure it with a pledge of equity rather than a property lien.

What is preferred equity?

Preferred equity investors receive returns before common equity holders but after all debt obligations are met. They usually receive a fixed return and may have limited upside participation.

What is common equity in a capital stack?

Common equity is the riskiest position but also has the highest potential return. These investors are paid last, after all debt and preferred equity, but they benefit from appreciation and profit sharing.

How does the capital stack affect risk and returns?

The higher you go in the stack, the more risk you take on, but also the greater the potential return. Senior debt has the least risk, while common equity carries the most.

What is a waterfall distribution in relation to the capital stack?

A waterfall outlines how cash flow is distributed among investors based on the capital stack. It ensures each layer is paid in order of priority before moving up to the next layer.

How can understanding the capital stack help me as an investor?

By analyzing the structure, you can assess whether a deal matches your risk tolerance and return goals. It also helps you understand where your money sits in priority during payouts or in the event of default.

Where can I learn more about applying the capital stack in multifamily deals?

Rod Khleif offers free resources, training, and live bootcamps that dive deep into capital stack structures and real-world examples. His programs are designed to help investors confidently finance and structure their multifamily deals.

Want to Learn More?

Explore expert insights on multifamily real estate investing, commercial real estate capital stack strategies, and financing solutions on Rod’s podcast.The #1 Multifamily Investing Event!

Ready to Build Your Multifamily Empire? 🚀

Rod Khleif’s Multifamily Bootcamp is the top event for serious investors. Network with expert investors who answer your questions and share proven strategies. Learn directly from industry leaders and take your investing to the next level!

🎟 Reserve Your Spot Now!

Related reading: For a complete overview of structures beyond conventional bank loans, including seller financing, master lease, sub-to, private money, JV, and syndication, read creative financing in real estate.

If you are leaning on government backed debt for this part of the stack, here is how to find an FHA multifamily lender.

Mismatching debt to your business plan is a fast way to lose money; review the 10 biggest mistakes new multifamily investors make before you finalize your capital stack.

Related reading: Real Estate Syndication Waterfall: How Profits Split