Multifamily financing is where most apartment deals are won or lost. It happens in the capital structure, not in talks or due diligence. Get it wrong and a perfectly good deal becomes a liability. Get it right and you can control multimillion-dollar assets with a fraction of the purchase price.

I’ve personally owned and managed over 2,000 properties across more than 40 years of investing. I’ve used almost every financing structure covered in this guide and I’ve watched investors win and lose money based on how well they understood their options.

This guide consolidates everything in one place: FHA loans, agency financing, bridge loans, the capital stack, and syndication equity. For a quick reference overview you can download and keep, grab our free Multifamily Financing resource.

Why Multifamily Financing Works Differently

Residential and multifamily financing are two different games. Understanding which rules apply determines how you structure every deal.

Properties of 1-4 units use residential financing. At 5 or more units, you enter commercial territory and commercial lenders underwrite the property’s Net Operating Income, not primarily your personal finances. This one difference changes everything:

- Loan approval is based primarily on NOI and Debt Service Coverage Ratio (DSCR), not your W2

- Down payments are typically 20% to 30% for commercial vs. 3.5% to 5% for FHA residential

- Your personal financial strength still matters : net worth and liquidity but the property carries the loan

- Non recourse structures are available, limiting your personal exposure. See our complete recourse vs. non recourse guide for the full breakdown.

|

Part 1: Residential Financing for 2 to 4 Unit Properties

FHA Loans : The Beginner’s On-Ramp

For investors buying a 2 to 4 unit property and willing to live in one unit, FHA multifamily loans are the most accessible entry point available. Backed by the Federal Housing Administration and HUD, these loans offer terms conventional investment loans can’t match.

- Down payment as low as 3.5% (580+ credit score)

- 30-year fixed rates for payment stability

- Lower rates than conventional investment property loans

- Seller can contribute up to 6% toward closing costs

- Owner-occupancy required: you must live in one unit for at least 12 months

This is the house hacking strategy and it’s one of the most powerful on ramps into multifamily. Your tenants offset the mortgage, often dramatically reducing or eliminating your housing cost. For the full case for starting here, read why your first home should be a multifamily property. And when you’re ready to find the right lender, see our guide to finding an FHA multifamily lender.

Conventional Residential Loans (1-4 Units, Non-Owner-Occupied)

For investors who don’t want to live in the property, conventional financing through Fannie Mae or Freddie Mac is available for 2 to 4 unit investment properties:

- Down payment: 15% to 25% depending on lender and loan size

- Credit score: 620 minimum, better rates at 740+

- No owner occupancy requirement

- Debt-to-income (DTI) limits apply based on your personal income

Once you’re ready to scale beyond 4 units, everything changes. See our complete guide to buying an apartment building for what the process looks like at 5 or more units.

Part 2: Commercial Financing for 5 or More Unit Properties

At 5 or more units you’re in commercial lending territory. Commercial lenders underwrite the property’s income first. Your loan amount is determined by DSCR (minimum 1.20x to 1.25x) and LTV (typically 65% to 75%). For the full lender perspective, read our guide to how a lender underwrites a multifamily loan.

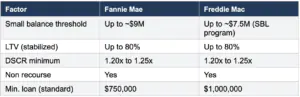

Agency Loans: Fannie Mae and Freddie Mac

Agency financing is the gold standard for stabilized multifamily. Fannie Mae and Freddie Mac purchase mortgages from approved lenders, enabling consistent, favorable terms at scale.

- Non recourse: personal assets protected from property underperformance (with standard fraud carve-outs)

- 30-year amortization, even on 5 to 10 year fixed terms

- Lowest available rates in multifamily : typically the benchmark other loan types are priced against

- LTV up to 75% to 80% on stabilized, well occupied assets

- Available for properties as small as 5 units through small balance programs

Agency loans require 90%+ occupancy for 90 days prior to closing. For value add deals that aren’t yet stabilized, bridge financing is required first.

Fannie Mae vs. Freddie Mac at a glance:

HUD/FHA Programs for 5 or More Units

Separate from residential FHA, HUD operates commercial multifamily programs for 5 or more unit properties through MAP approved lenders. These offer the most favorable terms in the market but at the cost of complexity and timeline. Learn more in our FHA multifamily loan guide.

- HUD 223(f): Purchase or refinance of existing stabilized properties. Up to 35-year fully amortizing, non recourse loans, LTV up to 83.3%

- HUD 221(d)(4): New construction or substantial rehabilitation. Up to 40-year terms, non recourse

- HUD 223(a)(7): Streamlined refinance of existing HUD-insured loans

HUD loans offer the longest terms and highest LTVs available but require 6 to 12 months to close and significant ongoing compliance. Best for long term hold strategies on stabilized assets.

Commercial Bank and Portfolio Loans

Community banks, regional banks, and credit unions offer multifamily loans held in their own portfolio : not sold to the GSEs. More flexible underwriting, but typically shorter terms.

- Recourse or non recourse depending on lender and deal size

- Loan terms: 3-10 years with 20-25 year amortization

- LTV: 65% to 75%

- Relationship-driven : your track record with the lender matters

- Faster closing than agency or HUD

- More flexibility for transitional assets or non-standard properties

Portfolio lenders are often the best option for your first commercial deal or for properties that don’t yet meet agency stabilization standards. Build relationships with 2 to 3 local commercial lenders before you need them.

CMBS Loans (Commercial Mortgage-Backed Securities)

CMBS loans are packaged into securities and sold to institutional investors. They offer competitive rates and high proceeds but come with significant structural inflexibility.

- Non recourse with standard carve-outs

- Fixed rates, typically 5 to 10 year terms, 30-year amortization

- Limited flexibility post-close : modifications, partial releases, or early payoff can be complex and expensive

- Best suited for stabilized institutional-quality assets with a clear hold to maturity plan

Part 3: Bridge Loans for Value Add Deals

Bridge loans are short term, higher rate financing designed for value add acquisitions for properties that aren’t yet stabilized enough for agency financing. If you’re buying to renovate and reposition, a bridge loan is typically your starting point.

- Term: 12 to 36 months with extension options

- Rate: typically 1% to 3% above agency rates (floating)

- LTV: 65% to 80% of as-is value

- Non recourse available from institutional bridge lenders

- Interest-only during the term to maximize cash flow during renovation

- Future funding draws for approved capital improvements in some programs

Bridge financing is intentionally temporary. The goal: acquire the property, execute the value add business plan, stabilize at 90%+ occupancy, then refinance into permanent agency debt. This progression is the foundation of the BRRRR strategy applied to multifamily for a full breakdown, see our BRRRR method for multifamily guide.

| Bridge vs. Agency: When to Use Each

Bridge: property below 90% occupancy, renovation planned, rents significantly below market, operational issues to resolve. Agency: property stabilized at 90%+ occupancy for 90+ days, rents at or near market, clean verifiable financials, longer-term hold intended. |

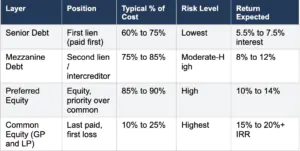

Part 4: The Capital Stack Explained

The capital stack is the layered structure of debt and equity used to finance a multifamily acquisition. Every layer has a different risk profile, return expectation, and priority of repayment. For the complete breakdown with worked examples, read our capital stack guide. Here’s the framework:

Senior Debt

The largest component : secured by a first lien on the property. If the deal fails, the senior lender is paid first. This security justifies the lowest cost in the stack. Most multifamily acquisitions are funded 60% to 75% by senior debt via the loan types covered above.

Mezzanine Debt

Sits between senior debt and equity. Secured by the borrower’s ownership interest in the holding entity rather than the property directly. Mezzanine fills the gap when senior debt doesn’t cover enough of the purchase price.

- Higher cost than senior debt due to subordinate position

- Lender can take over ownership interest if borrower defaults

- Common in larger institutional transactions : less typical below $10M deals

Preferred Equity

Sits above common equity in priority. Preferred equity investors receive a fixed return (typically 8% to 12%) before any profits flow to common equity investors. Unlike debt, there’s no set maturity date : though most structures include redemption provisions after a defined period.

- Used when senior loan plus mezzanine don’t fully cover capital requirements

- Common in syndications as an alternative to mezzanine when a second mortgage isn’t feasible

Common Equity (GP and LP Shares)

The riskiest position but the highest upside. Common equity investors are paid last in any distribution or liquidation. In a multifamily syndication, common equity is split between General Partners (GPs) who operate the deal and Limited Partners (LPs) who invest capital passively.

Part 5: Syndication Equity : How Investors Pool Capital

Syndication is how multifamily investors close deals larger than their personal capital allows and how passive investors access institutional real estate without operational involvement. For the complete framework, download the free Guide to Multifamily Syndications (220 pages, free).

GP and LP Roles

General Partner (GP): Finds the deal, arranges financing, manages due diligence and execution, oversees asset management. Contributes expertise and often 5% to 10% equity co investment.

Limited Partners (LPs): Passive capital investors. Contribute the majority of the equity. Receive a preferred return before profits are shared with the GP.

Common Return Structures in Syndications

- Preferred Return: LPs receive a fixed annual return (typically 6% to 8%) on invested capital before the GP earns any profit share.

- Equity Split: After preferred return, profits split between GP and LPs typically 70/30 or 80/20 in favor of LPs.

- Waterfall: Multi tier structure where the GP’s share increases as LPs hit higher return thresholds.

- GP Fees: Acquisition fees (1% to 2% of purchase price), asset management fees (1% to 2% of EGI annually), disposition fees (0.5% to 1% at sale).

SEC Compliance: 506(b) vs. 506(c)

Syndications are securities offerings regulated by the SEC. Most operators use one of two Regulation D exemptions:

- 506(b): Up to 35 non accredited (but sophisticated) investors plus unlimited accredited investors. No general solicitation. Pre existing relationship with investors required.

- 506(c): Unlimited accredited investors only. Public advertising and general solicitation allowed. Investor accreditation must be verified.

Always work with a qualified securities attorney when structuring a syndication. The legal structure protects both you and your investors.

| Free Resource

Download the free Multifamily Financing Overview a concise reference covering the capital stack, loan types, and key financing terms. Keep it on hand when evaluating deals or meeting with lenders. |

Part 6: Recourse vs. Non Recourse Financing

One of the most important structural decisions in multifamily financing. For the full comparison with worked examples, read our guide to recourse vs. non recourse multifamily financing.

| Factor | Recourse | Non Recourse |

|---|---|---|

| If you default… | Lender can pursue personal assets | Lender limited to the property only |

| Typical loan type | Community bank, portfolio loan | Agency, CMBS, institutional bridge |

| Deal size | Smaller ($500K-$5M) | Larger ($2M+) |

| Borrower experience req. | Lower : accessible for beginners | Higher : track record needed |

| Best for | First deals, local lenders | Scale, syndicators, investor capital |

Non recourse loans still include “bad boy” carve-outs that restore personal liability for fraud, intentional misrepresentation, or environmental violations. Non recourse protects you from market risk : not from misconduct.

Part 7: Qualifying for Commercial Multifamily Financing

Commercial lenders evaluate borrowers on four dimensions. Before approaching a lender, prepare accordingly. A current, complete personal financial statement is your financial handshake and lenders use it to verify net worth, liquidity, and existing obligations.

1. Net Worth

Most commercial lenders require net worth equal to or greater than the loan amount. A $3M loan requires $3M in net worth. For first-time commercial borrowers who don’t yet qualify individually, sponsors : experienced investors who co sign : can fulfill this requirement in exchange for a portion of the GP equity.

2. Liquidity

Post-closing liquidity: most lenders require liquid reserves equal to 10% of the loan amount after your equity contribution. On a $3M loan, you need $300,000 remaining in liquid assets. Liquid means cash or publicly traded securities : not real estate equity.

3. Experience

Agency and institutional lenders prefer borrowers with a track record of multifamily ownership. If you lack experience, partner with someone who has it. Experience requirements can be satisfied by your team, not just you individually : this is one of the primary advantages of working within a mentorship community.

4. The Property’s Performance

Commercial lenders ultimately lend on the property. If the NOI supports a 1.25x+ DSCR at your requested loan amount and LTV, strong deals can overcome borrower qualification gaps. Use our free multifamily deal analyzer to verify NOI and DSCR before approaching any lender.

Financing Strategy by Deal Stage: Quick Reference

| Deal Stage | Best Financing | Typical LTV | Key Requirement |

|---|---|---|---|

| House hack (2 to 4 units) | FHA residential | 96.5% | Owner-occupancy 12 months |

| Small MF, stabilized (5-30 units) | Portfolio / community bank | 65% to 75% | 90% occupancy, clean T-12 |

| Stabilized 30+ units | Agency (Fannie/Freddie) | 75% to 80% | 90%+ occupancy for 90+ days |

| Value add acquisition | Bridge loan | 65% to 75% as-is | Clear business plan, equity cushion |

| Long-term institutional hold | HUD 223(f) | Up to 83.3% | Stabilized, 35-yr amortization |

| Large syndicated deal | Agency + LP equity | Varies | SEC-compliant PPM, track record |

| Capital recycling (BRRRR) | Bridge then agency refi | Varies by stage | Stabilized NOI at refinance |

Creative Financing: No-Money-Down Structures

Not every acquisition requires a large personal down payment. For a comprehensive breakdown of strategies that minimize personal capital, see our guide to how to buy a multifamily property with no money.

- Seller Financing: The seller acts as the bank. Negotiate terms directly, eliminate traditional lender requirements. Best for motivated sellers with significant equity.

- Subject To: Take ownership while the seller’s existing loan stays in their name. Requires careful legal structure.

- Assumable Loans: Take over the seller’s existing FHA, VA, or commercial loan potentially at a below market rate. Powerful in today’s higher rate environment.

- Joint Ventures: Partner with someone who has capital or experience you lack. One party brings the deal, one brings the money.

- Private Money Lenders: Individual lenders at higher rates with less bureaucracy. Useful for acquisitions that don’t qualify for traditional financing or to move quickly.

Financing Readiness Checklist

Before approaching any commercial lender or investor, prepare these items:

- Personal Financial Statement: Current and complete. See the personal financial statement guide for what to include.

- Schedule of Real Estate Owned (SREO): every property, value, debt, equity, and income

- Trailing 12-month (T-12) income and expense statement for the subject property

- Current rent roll with unit-by-unit rents, lease terms, and occupancy

- Prior 2 to 3 years of tax returns (personal and business entities)

- Bank statements (2 to 3 months, all accounts)

- Property underwriting model: Complete NOI, DSCR, and return analysis. Use the free deal analyzer.

- Letter of Intent (LOI): Know what to include in a strong multifamily LOI before submitting an offer.

- Executive summary: 1 to 2 page overview of the deal, your background, and the business plan

- Phase I environmental report (if available)

| All Financing Resources in One Place

Free Financing Overview: rodkhleif.com/financing-your-multifamily-purchase/Capital Stack Deep Dive: Full guideFHA Loans for Investors: Full guideRecourse vs. Non Recourse: Full comparisonFree Deal Analyzer: Run the numbersMultifamily Underwriting Guide: Evaluate any dealFree Syndication Guide (220 pages): Download now |

Frequently Asked Questions: Multifamily Financing

1. What credit score do I need to get a multifamily loan?

For FHA residential loans (2 to 4 units, owner occupied): 580 minimum, though most lenders prefer 620+. For conventional investment loans: 620 minimum, significantly better rates at 740+. For commercial loans (5 or more units): most lenders want 680+, and agency programs typically require 680-700+. In commercial underwriting, your credit score is one factor among many and the property’s NOI and your net worth are weighted equally or more heavily.

2. How much do I need to put down on an apartment building?

It depends entirely on the strategy and loan type. FHA owner occupied (2 to 4 units): 3.5% down. Conventional investment property (2 to 4 units): 15% to 25%. Commercial portfolio loan (5 or more units): 20% to 35%. Agency financing (stabilized 5 or more units): 20% to 25%. Bridge loans: 25% to 35%. In a syndicated deal, the GP’s personal down payment may be just 5% to 10%, with the balance raised from LP investors.

3. What is DSCR and why does every lender focus on it?

DSCR (Debt Service Coverage Ratio) measures the property’s NOI relative to its annual debt payments. A 1.25x DSCR means the property earns 25% more than needed to service the loan. Most commercial lenders require a minimum 1.20x to 1.25x DSCR. If your underwritten NOI doesn’t produce sufficient DSCR at the target loan amount, either your purchase price needs to come down or your value add plan must deliver stronger income. Use the free deal analyzer to test your DSCR on any deal before approaching a lender.

4. What’s the difference between a bridge loan and agency financing?

Bridge loans are short term (12 to 36 months), higher rate financing for value add acquisitions that aren’t yet stabilized. They allow you to acquire, renovate, and stabilize a property. Agency financing (Fannie Mae, Freddie Mac) is long term, lower rate permanent financing for stabilized properties at 90%+ occupancy. The typical progression: acquire with bridge, execute the business plan, stabilize, then refinance into agency. This is also the core of the BRRRR method applied to multifamily.

5. Can I get non recourse financing as a first-time commercial borrower?

Possibly but it’s challenging. Non recourse agency and institutional lenders want to see a track record. Options for first timers include: partnering with an experienced sponsor who satisfies the experience and net worth requirements; starting with a recourse portfolio loan and building toward agency on your next deal; or participating in a joint venture led by an experienced operator to build your track record. Experience requirements can be satisfied by your team, not just you individually.

6. How does HUD 223(f) differ from standard FHA multifamily loans?

They are completely different programs. Residential FHA loans (2 to 4 units) are consumer mortgage products for owner occupants with 3.5% down. HUD 223(f) is a commercial multifamily program for 5 or more unit properties, offering up to 83.3% LTV, 35-year fully amortizing non recourse financing, and among the lowest long term rates available but with 6 to 12 month closing timelines and ongoing compliance requirements. Find a qualified MAP approved HUD lender if you’re pursuing this path.

7. What is preferred equity and when is it used in a deal?

Preferred equity sits between debt and common equity in the capital stack. Preferred equity investors receive a fixed return (typically 8% to 12%) before any profits flow to common equity (GPs and LPs). It’s used when senior debt doesn’t cover enough of the capital requirement and mezzanine debt isn’t available or practical. In syndications, some GPs raise a tranche of LP equity structured as preferred equity to provide investors priority distributions.

8. What does the lender actually need from me to approve a commercial loan?

The four primary factors are: (1) the property’s NOI and DSCR, (2) your net worth and liquidity via a current personal financial statement, (3) your track record of managing income properties, and (4) the quality of the market and asset. For a full breakdown of what the lender reviews and how to prepare your package for approval, see our guide on how a lender underwrites a multifamily loan.

9. Can I use a self-directed IRA or 401(k) to invest in multifamily?

Yes. Self-directed IRAs (SDIRAs) can invest in real estate : including multifamily properties and syndications : through a custodian that permits alternative assets. Passively investing as an LP in a syndication through an SDIRA is common and relatively straightforward. Active involvement as a GP can trigger Unrelated Business Taxable Income (UBTI) and may complicate the tax treatment. Always work with a CPA experienced in real estate before deploying retirement funds into any deal.

10. What’s the best first step if I’ve never financed a multifamily deal before?

Start with the fundamentals: understand how commercial underwriting works, what drives NOI, and how the capital stack is structured. Then download the free Multifamily Financing Overview and build relationships with 2 to 3 local commercial lenders before you have a deal. Get your personal financial statement in order and run the numbers on live deals using the free deal analyzer. The clearer your financial picture and the stronger your deal analysis, the more confident your first lender conversation will be.

Ready to Finance Your First (or Next) Multifamily Deal?

Financing is learnable. Every experienced multifamily investor started without a track record, without lender relationships, and without certainty about which structure fit their strategy. What separated the ones who succeeded was education, preparation, and consistent action.

Start here: download the free Multifamily Financing Overview a concise reference you can keep on hand for every deal. When you’re ready to go deeper on deal analysis, underwriting, and structuring your first acquisition, join me at the next Multifamily Bootcamp or grab Rod’s free best-selling book: How to Create Lifetime Cash Flow Through Multifamily Properties.