I’ve purchased dozens of apartment buildings, and I can tell you the process is 80% preparation and 20% execution. Buying an apartment building isn’t mysterious. You choose a target market, find deals, review the numbers, and secure financing before closing. But here’s where most people mess up: they skip steps or rush the underwriting because they’re desperate to own their first property. I refined a step-by-step system that removes risk and maximizes returns at every stage. Let me take you through each stage so you walk in knowing exactly what to expect. Most people assume buying an apartment building is reserved for institutions and insiders with deep pockets. That’s not how it works. I’ve owned over 2,000 properties. I’ve seen thousands of my students close their first multifamily deals. Many did it without using their own money.

This guide tells you exactly how to do it in 2026. We’ll cover every step from market selection to closing day, plus what’s actually different about the current environment and how to use it to your advantage.

Is Buying an Apartment Building Worth It in 2026?

Yes, and the timing may be better than it’s been in several years. Here’s the honest picture of where the market stands right now.

The multifamily sector went through a painful correction between 2022 and 2024 as interest rates spiked and cap rates expanded. That pain created opportunity. Sellers who were unrealistic about pricing have adjusted. Construction starts have slowed dramatically, which means new supply coming online through 2026 and 2027 will be limited. Rental demand, meanwhile, remains structurally strong: home prices are still elevated, mortgage rates are still above 6%, and household formation continues.

That combination limited new supply, sticky rental demand, motivated sellers, and easing credit conditions is historically a favorable setup for buyers.

“Multifamily is not a get rich quick strategy. It’s a get wealthy certainly strategy. The investors who win are the ones who buy well, operate well, and stay patient.” Rod Khleif

Beyond market timing, the structural case for apartment buildings is straightforward. You get multiple income streams from one asset, commercial financing that scales with the property’s performance rather than just your personal income, and the ability to force appreciation by improving operations something you can’t do with stocks or single family homes valued entirely by comparable sales.

If you’re weighing apartments against houses, read our full breakdown on whether apartment buildings are a good investment before going further.

What You’re Really Buying When You Buy an Apartment Building

This framing matters more than almost anything else in this guide: when you buy an apartment building, you are not buying real estate. You are buying a business.

That business has:

- Revenue: rent, laundry, storage, parking, pet fees

- Operating expenses: management, maintenance, insurance, taxes, utilities

- Employees: property managers, maintenance staff, leasing agents

- Customers: your tenants

- A valuation method tied directly to income, not comparable sales

That last point is the most important. Unlike a single family home where your neighbors’ sale prices determine your value, a multifamily building is valued based on its Net Operating Income (NOI). Every dollar you add to NOI by raising rents, reducing expenses, or adding income streams directly increases the value of the building. This is called forced appreciation, and it’s one of the most powerful wealth building mechanisms in real estate.

Think like a business owner, not a homeowner, and you’ll be ahead of 90% of the investors you’re competing with.

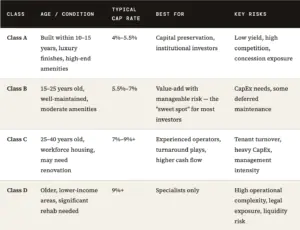

Understanding Property Classes: A, B, C, and D

Every apartment building falls into one of four classes. Understanding these helps you match your strategy to your experience level, capital, and risk tolerance.

For most first time buyers, a Class B or stabilized Class C property offers the best balance of affordability, upside, and manageable risk. You have room to add value without the extreme operational challenges of a D-class turnaround.

To understand how class affects what you should pay, see what a good cap rate looks like for each class.

How to Pick the Right Market

The right building in the wrong market will underperform. The right market with a mediocre building can still produce strong results. Market selection is that important.

These are the four fundamentals I look at every time:

1. Job Growth

Jobs are the engine of rental demand. Look for markets attracting major employers in 2026, that means logistics and distribution, healthcare, advanced manufacturing, and tech. When Amazon, a major hospital system, or a new corporate campus announces expansion, rental demand follows within 12 to 24 months.

2. Population Trends

People vote with their feet. Markets gaining population consistently particularly working age adults aged 25 to 44 tend to have lower vacancy rates and stronger rent growth. Sun Belt markets and secondary metros in the Southeast and Mountain West continue to attract migration in 2026.

3. Supply Pipeline

This matters more than most investors realize. Check how many new apartment units are under construction or permitted in your target submarket. Markets with heavy new supply can see rent growth stall or reverse even when overall demand is strong, because tenants have newer options. In 2026, the supply hangover from 2021 to 2023 construction is washing through many major metros understanding where it’s concentrated helps you avoid the worst pockets.

4. Rental Demand Indicators

Look at current vacancy rates (under 6% is healthy), trailing 12 month rent growth, and how quickly units lease. If apartments in your target area are absorbing quickly and rents are trending up, that’s your signal.

Rod’s Rule

Before you fall in love with a building, fall in love with the fundamentals of its submarket. The best deal on a bad block is still a bad deal.

How to Buy an Apartment Building: Step by Step

Whether you’re buying a 6 unit or a 60 unit, the process follows the same proven path. Here it is in full.

Build Your Power Team

Multifamily is a team sport. Before you look at a single property, get the right people in place:

- Multifamily broker who specializes in your target market and asset class

- Commercial lender or mortgage broker experienced in apartment financing

- Property manager even if you plan to self manage initially, interview several now

- Real estate attorney who handles commercial transactions

- CPA who understands depreciation, cost segregation, and 1031 exchanges

Your team determines your deal flow, your underwriting quality, and your ability to close. Cheap out here and you pay for it everywhere else.

Get Pre Approved or Prepare Your Capital Raise

You need to know your buying power before you make offers. For conventional financing, get a pre approval letter from a commercial lender and prepare your personal financial statement and schedule of real estate owned.

If you plan to raise capital from other investors through a multifamily syndication, start building your investor list, preparing your pitch materials, and studying SEC compliance guidelines now not after you’re under contract.

You don’t need all the money yourself. Partnerships, joint ventures, and syndications are how most larger deals get done.

Analyze Deals Like a Professional

Get in the habit of underwriting deals daily even before you’re ready to buy. The more deals you analyze, the sharper your instincts become. Use these four core metrics on every property:

- Cap Rate NOI ÷ Purchase Price. Use our free cap rate calculator to run numbers instantly.

- NOI (Net Operating Income) Gross income minus all operating expenses, before debt service.

- Cash on Cash Return Annual pre tax cash flow ÷ Total cash invested.

- DSCR (Debt Service Coverage Ratio) NOI ÷ Annual debt service. Lenders want to see 1.25x or higher.

Use the free Commercial Real Estate Underwriting Tool to run a complete analysis before making any offer.

Submit a Letter of Intent and Negotiate

When you find a deal that pencils out, move quickly. Start with a Letter of Intent (LOI) that outlines your price, terms, due diligence period, and closing timeline. The LOI is non binding but sets the tone for the entire negotiation.

Once the LOI is accepted, your attorney drafts the Purchase and Sale Agreement (PSA). Negotiate firmly but professionally and always leave room for renegotiation after due diligence uncovers issues.

Conduct Due Diligence

Due diligence is where many deals get repriced or walked away from entirely. Don’t rush it. Verify every assumption the seller gave you.

Key items to review:

- Rent roll (current tenants, unit mix, lease terms, deposits)

- Trailing 12 month (T12) income and expense statements

- Unit by unit physical inspection

- All existing leases and any tenant disputes

- Title, zoning, and legal compliance

- CapEx needs: roof, HVAC, plumbing, electrical, parking

- Insurance history (especially claims)

- Environmental concerns (asbestos, lead paint, Phase I ESA)

Download our complete multifamily due diligence guide for the full checklist.

Close and Execute Your Business Plan

Closing day is not the finish line it’s the starting gun. The moment you take ownership, your business plan kicks into gear.

- Implement planned renovations on a timeline tied to lease expirations

- Adjust rents to market (where leases allow)

- Onboard your property management team and systems

- Audit all expenses and eliminate waste

- Add ancillary income streams: storage, parking, laundry, RUBS

Track your KPIs weekly. Treat this like the business it is.

Financing Options for Buying an Apartment Building in 2026

Financing a 5+ unit building is fundamentally different from getting a home mortgage. The lender’s primary question is not “how much do you make?” it’s “how much does the property produce?” This actually works in your favor as your portfolio grows.

Here are the main loan types available to apartment building buyers in 2026:

Conventional Commercial Bank Loans

The most common starting point. Local and regional banks typically offer 5 to 10 year fixed rate terms with 20 to 30 year amortization schedules. They require strong personal credit (680+), 25 to 30% down, and will scrutinize the property’s financials carefully. These are relationship driven loans a good commercial banker who knows your market is worth developing early.

Agency Loans (Fannie Mae / Freddie Mac)

For properties with 5+ units, Fannie Mae and Freddie Mac offer some of the most competitive rates and terms in the market. They require stabilized occupancy (usually 90%+), are typically non recourse above certain thresholds, and can offer 10 to 30 year fixed terms. The application process is more rigorous, but the terms are often worth it for stabilized assets.

FHA / HUD Loans

For 2 to 4 unit properties where you owner occupy one unit, FHA loans allow as little as 3.5% down making them one of the best entry points for new investors. For larger properties, HUD’s 221(d)(4) and 223(f) programs offer long term, fully amortizing, non recourse financing at competitive rates, though the process is more time intensive.

Bridge Loans

Short term, interest only loans used to acquire value add properties that don’t yet qualify for permanent financing due to low occupancy or deferred maintenance. Once you stabilize the property, you refinance into permanent debt. Bridge loans come with higher rates (typically 1 to 3% over SOFR) but give you the flexibility to close on properties that need work.

Seller Financing

In the current environment, motivated sellers are more open to carrying a note than they’ve been in years. This can dramatically reduce or eliminate the need for institutional financing. Always have your attorney review seller financed deals carefully.

Syndication (Other People’s Money)

For larger deals, you can raise equity capital from passive investors while you serve as the General Partner. You find and operate the deal; investors provide the equity. This allows you to control assets far beyond what your personal capital could finance. Learn how multifamily syndication works if you want to scale into larger assets.

For a complete breakdown of how to buy a multifamily property with little or no money of your own, see our guide on buying multifamily with no money down.

How Much Does It Cost to Buy an Apartment Building?

The total capital required to close a deal has four components: down payment, renovation budget, closing costs, and operating reserves. Here’s how each breaks down.

| Cost Component | Typical Range | Notes |

| Down Payment | 20%–30% of purchase price | Can come from your own funds, partners, or syndication investors |

| Renovation / CapEx | $3,000–$15,000+ per unit | Varies widely by property condition and scope of value add plan |

| Closing Costs | 2%–5% of purchase price | Includes legal fees, appraisal, inspection, title, loan origination |

| Operating Reserves | 6 to 12 months PITI | Lenders often require this; always smart to have regardless |

Sample Breakdown: $2.5M, 30 Unit Building

- 25% down payment: $625,000

- CapEx budget (value add): $150,000

- Closing costs (~3%): $75,000

- Operating reserves: $60,000

- Total capital required: ~$910,000

That $910K doesn’t need to come from you alone. Many investors bring in equity partners or raise funds through a syndication to reach the capital requirement. Your job is to find the deal, underwrite it, and structure it correctly.

How to Underwrite an Apartment Building Deal

Underwriting is simply answering two questions: what is this property worth today, and what can I make it worth? Here’s the framework I use.

Step 1: Build the Pro Forma Income Statement

Start with the rent roll to determine Gross Potential Rent (GPR) what the property would collect if every unit was leased at full market rent. Then subtract vacancy (typically 5 to 10%) and add any ancillary income (laundry, storage, parking) to get Effective Gross Income (EGI).

Step 2: Calculate NOI

Subtract all operating expenses from EGI. Do NOT include debt service in this calculation. NOI is a pre financing metric, which is what makes it powerful for comparison across deals. Operating expenses typically run 35 to 50% of EGI on a well run property.

Step 3: Determine Value via Cap Rate

Divide NOI by the prevailing market cap rate for that asset class and market. This gives you the income based value: Value = NOI ÷ Cap Rate. Use our free cap rate calculator to run this instantly.

To understand how cap rates work with real examples, including how rising rates affect valuation, read our deep dive guide.

Step 4: Stress Test Your Assumptions

Run a downside scenario: what happens if rents come in 5% below projection? If vacancy runs at 10% instead of 5%? If insurance costs spike 20%? If the deal only works under perfect conditions, it’s not a deal worth doing.

Step 5: Model Your Exit

Know your exit before you buy. If you’re planning a 5 year hold and sale, model what the property will be worth at exit using your projected NOI at year 5 and a conservative exit cap rate (typically 0.25%–0.5% higher than your going in cap to account for market risk).

Free Tool

Use the Free Commercial Real Estate Underwriting Tool →

Run a complete income, expense, financing, and return analysis on any deal in minutes.

Due Diligence Checklist for Apartment Buildings

Due diligence is where assumptions meet reality. Approach it systematically and without emotion. These are the areas you must verify before releasing contingencies.

Financial Due Diligence

- Trailing 12 month (T12) income and expense statements

- Current rent roll with lease start/end dates, rent amounts, deposits

- Bank statements confirming actual income collected (not just what’s on the P&L)

- Current and prior year property tax bills

- Insurance declarations page and claims history

- All existing service and vendor contracts

- Utility bills (last 12 months)

Physical Due Diligence

- Third party property inspection (structural, electrical, plumbing, HVAC)

- Roof age and condition report

- Unit by unit walkthrough with condition notes

- Common areas, parking, laundry, amenities

- Phase I Environmental Site Assessment (for most commercial loans)

- Asbestos and lead paint assessment if building is pre 1978

Legal and Title Due Diligence

- Title search and title insurance commitment

- Survey (confirm boundaries and encroachments)

- Zoning verification and certificate of occupancy

- Review of all existing leases and tenant agreements

- Outstanding permits, code violations, or litigation

- HOA documents (if applicable)

For the full checklist and a step by step walkthrough, download our free guide to multifamily due diligence.

Common Mistakes When Buying an Apartment Building

I’ve made expensive mistakes. My students have made expensive mistakes. Here are the ones that come up most often so you don’t have to repeat them.

Trusting the Seller’s Numbers Without Verification

Sellers present their properties in the best possible light. Always verify income against bank statements and actual lease documents not just the pro forma they handed you. Many investors have bought properties where the “current rents” on the rent roll were months old asking rents on vacant units.

Underestimating CapEx

Most first time buyers underestimate the cost and scope of capital expenditures. Get a third party inspection report before you finalize your offer, and budget conservatively. A roof you thought had five years left may have two.

Buying the Deal Instead of the Market

A great price on a bad property in a declining submarket is still a bad deal. Always evaluate the market first, then the deal.

Inadequate Reserves

Running out of reserves is one of the most common reasons investors lose properties. Build in at least six months of PITI, plus a CapEx reserve. If a lender doesn’t require it, still do it.

No Clear Business Plan

Buying without a specific, executable business plan rent projections, CapEx timeline, management strategy, and exit is speculation, not investing.

Skipping Professional Property Management

Self managing a multifamily property without experience is one of the fastest ways to destroy returns. Hiring the right property manager is one of the most important decisions you’ll make.

Apartment Buildings vs. Single Family Homes: The Real Comparison

If you’re currently investing in single family homes or considering it here’s the honest comparison.

| Factor | Single Family | Apartment Building |

| Vacancy risk | 100% income loss on 1 vacancy | Spread across multiple units |

| Valuation method | Comparable sales (you don’t control) | Income based (you can force appreciation) |

| Financing | Personal income–dependent | Property performance–dependent |

| Scalability | One unit per transaction | Multiple units per transaction |

| Management | Spread across multiple locations | Concentrated, more efficient |

| Tax advantages | Standard depreciation | Accelerated depreciation, cost segregation, 1031 |

| Entry barrier | Lower | Higher but more scalable |

Multifamily’s core advantage is that every lever you pull to improve the business directly improves the asset’s value. No amount of landscaping at a single family home will increase its appraised value if comparable homes in the neighborhood haven’t moved.

How to Buy an Apartment Complex With Little or No Money Down

The question I get more than any other: can you buy an apartment complex without writing the whole check yourself? Yes, and it is how most of the operators I know got started. You are not borrowing your way to a down payment. You are trading something you have for capital someone else has.

Four structures that actually work in 2026:

- Syndication. You find the deal, underwrite it, and raise the equity from investors who want passive returns. You earn ownership for sourcing and operating the asset. This is the most common path to a first large apartment complex.

- Joint venture partnership. One partner brings capital, the other brings the deal, the experience, and the day to day work. Cleaner than a syndication on smaller deals because you avoid the securities complexity.

- Seller financing. An owner who has held the property for decades and owns it free and clear often cares more about monthly income and taxes than a lump sum. A seller carry can sharply reduce the cash you bring to closing.

- Assuming existing debt. When in place debt carries a below market rate, assuming it can be worth more than any discount on price, and it lowers the equity you need to close.

What none of these remove is the need to be credible. Lenders and investors still look for net worth, liquidity, and experience somewhere on the sponsorship team. If you do not have it yet, partner with someone who does and give up a slice of the deal. Owning 30 percent of a real apartment complex beats owning 100 percent of a deal you never closed.

Be honest about the tradeoff: every dollar you do not bring is ownership, control, or upside you give away. That is a fair trade on your first deal and an expensive habit by your fifth.

Frequently Asked Questions: How to Buy an Apartment Building

How do I buy an apartment complex with no money down?

“No money down” usually means structuring the deal so none of the required capital is yours not that the capital doesn’t exist. Common strategies include bringing in equity partners (you provide the deal, they provide the capital), using multifamily syndication, negotiating seller financing, or assuming existing debt.

For 2 to 4 unit properties, FHA loans allow as little as 3.5% down if you owner occupy one unit. On larger deals, the capital requirement is real your job is to find it and structure the deal correctly. See our full guide on buying multifamily with limited capital.

What credit score do I need to buy an apartment building?

For residential loans on 1 to 4 unit properties, FHA requires a minimum 580 score for 3.5% down. For commercial loans on 5+ unit buildings, most lenders want 680+ but the property’s DSCR matters as much as your personal credit. If your credit is below that threshold, a strong co borrower or guarantor can bridge the gap, and most deals are structured with partners whose combined credentials satisfy the lender.

How long does it take to buy an apartment building?

From accepted offer to close typically runs 45 to 90 days for conventional and bridge financing. Agency loans (Fannie/Freddie) can take 60 to 90 days; HUD loans can take 6 to 12 months. Factor this into your earnest money negotiations if you need more time for due diligence or financing, negotiate for it in the PSA.

How do I find apartment buildings for sale?

The best deals rarely appear on public listing sites first. Build relationships with multifamily brokers who specialize in your target market and tell them your exact buy box. Supplement that with direct mail campaigns to owners of properties in your target size range, networking at local real estate investment associations (REIAs), and using county records to identify long term owners who may be motivated to sell. Off market deals sourced through broker relationships and direct outreach are where the best opportunities typically hide.

Do I need a real estate license to buy an apartment building?

No. You need a license to represent other people in transactions and earn commissions. As an investor purchasing for your own portfolio, no license is required. What you need is the right team: a licensed multifamily broker, commercial lender, and real estate attorney to handle the licensed activities while you focus on the investing.

Is 2026 a good time to buy an apartment building?

The conditions entering 2026 are more favorable for buyers than they’ve been in several years. Sellers have adjusted from peak-2021 pricing expectations, credit conditions are easing, new supply coming online is slowing (the 2021 to 2023 construction wave is working through the pipeline), and rental demand remains structurally strong due to elevated home prices and elevated mortgage rates keeping would be homebuyers in the rental pool. That said, submarkets vary significantly some are oversupplied, some are tight. Market selection is the critical variable.

How do I analyze an apartment building before buying?

Start with the four core metrics: cap rate (use the free calculator), NOI, cash on cash return, and DSCR. Then verify those numbers against the actual rent roll, trailing 12 month financials, and a physical inspection. Stress test your assumptions model what happens if rents come in 5% below projection and vacancy runs 2% higher. Use the free Commercial Real Estate Underwriting Tool to run a complete analysis.

You’re Closer Than You Think

Every seasoned investor you admire started exactly where you are asking the same questions, feeling the same uncertainty. The difference is they took a step.

Buying an apartment building creates cash flow, forced appreciation, tax advantages, and long term wealth. It is one of the most proven paths to financial independence that exists. The process is learnable. The capital is findable. The deals are out there.

You’re one deal away from Lifetime Cashflow.

Disclaimer: This article was written with the assistance of AI and reviewed by Rod Khleif and his team for accuracy and relevance. This is for informational purposes only and does not constitute financial, legal, or investment advice. Always consult qualified professionals before making investment decisions.

Ready to Buy Your First (or Next) Deal?

Get Rod’s best selling book free, join the next Multifamily Bootcamp, or apply for the Warrior Program.

Disclaimer: This article was created with the assistance of AI and reviewed by Rod Khleif and his team to ensure accuracy and relevance.