Most real estate investors know the BRRRR method from the single-family world. But here’s what few people talk about: when you apply the BRRRR strategy to multifamily real estate, the returns compound in ways that single-family investing simply can’t match.

I’ve helped thousands of students build multifamily portfolios from scratch. When done right, the BRRRR method is a powerful framework. It helps them scale fast, recycle capital, and build long-term cash flow.

In this guide, I’ll break down exactly what the BRRRR method is, how it works differently with apartment buildings, step-by-step how to execute it, and the mistakes I see investors make that cost them real money.

| What You’ll Learn in This Guide

What BRRRR stands for and how it works in multifamily | How to find the right value-add apartment deals | Step-by-step execution from acquisition to refinance | Key metrics to evaluate a BRRRR multifamily deal | Common mistakes and how to avoid them | How to scale from one BRRRR deal to a full portfolio |

What Is the BRRRR Method?

BRRRR stands for:

- Buy

- Rehab

- Rent

- Refinance

- Repeat

The strategy works like this: You buy a distressed or underperforming property below market value. You raise its value with renovations and better management. You stabilize it by filling it with tenants. Then you do a cash-out refinance to pull out your invested capital. You use that capital to fund the next deal.

Done well, BRRRR allows you to recycle the same pool of capital across multiple deals rather than leaving it permanently locked in a property.

|

Why BRRRR Works Differently in Multifamily

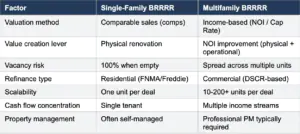

In single-family real estate, BRRRR works primarily through comparable sales (comps). You renovate to increase the property’s market value relative to neighboring homes.

In multifamily, valuation is income-based. A commercial lender doesn’t care what the house next door sold for. They care about one thing: Net Operating Income (NOI).

Multifamily value is calculated as: Value = NOI ÷ Cap Rate

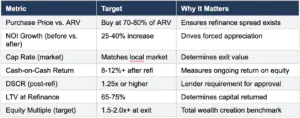

This means every dollar of NOI you add creates a multiplied increase in property value. In a market with a 6% cap rate, adding $10,000 in annual NOI increases property value by roughly $167,000. That’s the leverage point BRRRR investors in multifamily use to manufacture equity at scale.

| Example

You buy a 24-unit apartment building with below-market rents and mismanaged expenses. NOI at acquisition: $120,000. After rehab and rent increases, NOI grows to $180,000. At a 6% cap rate, the property value jumps from $2,000,000 to $3,000,000 — a $1,000,000 increase. Now you refinance against that new value and pull your capital back out. |

Step-by-Step: How to Execute the BRRRR Method in Multifamily

Step 1: Buy the Right Property

Not every multifamily deal is a BRRRR candidate. You need a value-add opportunity — a property where the current owner has left money on the table. Look for:

- Below-market rents (existing tenants paying significantly less than market rate)

- High vacancy due to deferred maintenance or poor management

- Bloated operating expenses that can be trimmed

- Mismanaged properties owned by tired or out-of-state landlords

- Properties in markets with strong rent growth fundamentals

Your purchase price must leave enough spread between acquisition cost and after-repair value (ARV) to support a cash-out refinance. Most experienced investors target buying at 70-80% of stabilized value.

Key metric to verify before buying: After-Repair NOI ÷ Cap Rate > (Purchase Price + Rehab Cost + Closing Costs)

Step 2: Rehab to Force Appreciation

In multifamily BRRRR, rehab has two dimensions: physical and operational.

Physical improvements that justify rent increases:

- Unit interiors: new flooring, appliances, cabinets, fixtures

- Common areas: landscaping, lighting, signage, laundry rooms

- Mechanical systems: HVAC, plumbing, roofing if deferred

- Curb appeal upgrades that support premium positioning

Operational improvements that increase NOI:

- Replace underperforming property management

- Audit and renegotiate vendor and service contracts

- Implement utility billing back to tenants (RUBS program)

- Add revenue streams: storage units, covered parking, pet fees

- Lease up vacant units to market rents

The operational side is where most BRRRR investors in multifamily leave money on the table. Physical renovations get the press, but trimming $30,000 in unnecessary expenses creates the same NOI impact — and the same value increase — as a full unit renovation program.

Step 3: Rent to Stabilize

Before a lender will refinance your apartment building, they need to see stabilized occupancy. Most lenders require 90% occupancy for 90 days before they’ll order an appraisal.

During the stabilization period:

- Fill vacant units at market rate (not discounted to fill quickly)

- Renew existing leases at market rate as they expire

- Document all income and expenses with clean T-12 financials

- Maintain consistent occupancy — don’t rush the lease-up at the expense of tenant quality

| Pro Tip

Lenders look at your trailing 12-month (T-12) income statement to verify NOI. Start keeping immaculate records from day one. The cleaner your financials, the smoother your appraisal and refinance process. |

Step 4: Refinance to Recycle Capital

Once the property is stabilized, you order a new appraisal based on the improved NOI. A commercial appraiser will use the income approach to calculate current value. If your value creation plan worked, the appraisal will come in significantly higher than your all-in cost.

With the new appraised value established, you apply for a cash-out refinance. Most commercial lenders will lend up to 70-75% loan-to-value (LTV) on a stabilized multifamily property.

| Refinance Math Example

All-in cost (purchase + rehab + closing): $1,800,000Stabilized value at refinance: $3,000,000Loan at 70% LTV: $2,100,000Original acquisition loan payoff: $1,350,000Cash returned to you: $750,000If your original equity invested was $600,000, you’ve returned all your capital plus $150,000 — while still owning the building free and clear of personal equity. |

The goal isn’t always to pull out 100% of your capital. It’s to pull out enough to fund your next deal while keeping the property cash flow positive with the new, higher loan balance.

Step 5: Repeat to Build Your Portfolio

The capital you’ve recycled from the refinance now becomes the equity for your next BRRRR deal. This is how investors scale from 20 units to 200 units — not by saving more money, but by engineering deals that give their capital back.

Each completed BRRRR deal adds:

- A cash-flowing asset you own with minimal equity trapped

- Principal paydown from tenants over time

- Long-term appreciation on a stabilized, well-managed property

- Recycled capital to fund the next acquisition

Key Metrics for Evaluating a Multifamily BRRRR Deal

BRRRR Multifamily vs. BRRRR Single-Family: Key Differences

Common BRRRR Mistakes (and How to Avoid Them)

Mistake #1: Overestimating After-Repair Value

Investors often build their BRRRR spreadsheet backward — deciding what they want the refinance to look like, then reverse-engineering assumptions to make the numbers work. Always underwrite conservatively. Use market cap rates, not best-case scenarios. Get a broker opinion of value before you close.

Mistake #2: Underestimating Rehab Costs

Deferred maintenance on a 40-unit building can be catastrophic to your budget if you miss it in due diligence. Get a full property inspection, a systems report (roof, HVAC, plumbing, electrical), and contractor bids before closing. Add a 15-20% contingency to whatever number you land on.

Mistake #3: Not Accounting for Stabilization Time

Most lenders want 90 days of stabilized occupancy before refinancing. But lease-up can take longer than planned. Budget for 6-12 months of carrying costs (mortgage, insurance, taxes, utilities) from acquisition to refinance. Running out of cash mid-execution is the most common way a BRRRR deal fails.

Mistake #4: Refinancing Into Negative Cash Flow

The whole point of BRRRR is to keep a cash-flowing asset while recycling your capital. If the refinanced loan amount is so high that debt service exceeds NOI, you’ve traded equity for a liability. Your DSCR after refinance should be at least 1.25x — meaning the property generates 25% more NOI than it needs to cover debt service.

Mistake #5: Using BRRRR Without Understanding Financing Options

The refinance is the engine of BRRRR. Before you buy, know exactly which lender will refinance the property, under what conditions, at what LTV, and on what timeline. Get pre-qualified for the refi before you close on the acquisition. Surprises in the financing step can strand your capital for years.

Is BRRRR Right for You? Who This Strategy Works For

The BRRRR method for multifamily works best for investors who:

- Have access to capital (either personal, private lender, or bridge financing) to fund the acquisition and rehab before refinancing

- Are comfortable with value-add execution — project management, contractor oversight, property management transitions

- Have a strong understanding of commercial underwriting and NOI-based valuation

- Are willing to operate in the 12-36 month timeframe a full BRRRR cycle typically requires

- Have a clear lender relationship in place before buying

If you’re newer to multifamily investing, BRRRR is achievable — but it’s more complex than a standard acquisition. Many of my Warrior students execute their first BRRRR deal after starting with a smaller stabilized property to build experience, relationships, and credibility with lenders.

| Next Step

If you’re serious about executing a multifamily BRRRR deal, the foundation is understanding how to underwrite value-add properties accurately. Download Rod’s free Multifamily Investing book or join the next Multifamily Bootcamp to learn the full underwriting and deal execution framework. |

Frequently Asked Questions About BRRRR Multifamily Investing

Can you BRRRR a large apartment complex?

Yes — in fact, the BRRRR method scales more efficiently with larger properties. A 50-unit building has more levers for NOI improvement than a duplex, and commercial financing is available for properties of all sizes. Many syndicators use a BRRRR-style strategy across 100+ unit acquisitions, often using bridge loans to fund the acquisition and rehab before refinancing into agency or permanent financing.

What type of financing do you use to buy the property initially?

Common options include bridge loans (short-term, higher-rate commercial financing designed for value-add), hard money lenders, private equity partners, or seller financing. The acquisition financing is intentionally temporary — the refinance into long-term permanent financing is the goal.

How long does a multifamily BRRRR cycle typically take?

Plan for 12-24 months from acquisition to refinance on a typical value-add multifamily BRRRR. Rehab can take 3-9 months depending on scope, and lenders typically require 90 days of stabilized occupancy before refinancing. Factor in time for the refinance process itself (60-90 days).

What if the appraisal comes in lower than expected?

This is the most common BRRRR risk. If the appraisal comes in low, you may not be able to pull out as much capital as planned — or any capital at all. Mitigate this by underwriting conservatively, building in a margin of safety between your all-in cost and your projected ARV, and getting a broker opinion of value before closing on the acquisition.

Can you use syndication to fund a multifamily BRRRR deal?

Absolutely. Many syndicators use investor equity to fund the acquisition and rehab, then refinance to return investor capital (or a portion of it) and extend the hold. This structure allows you to scale BRRRR deals without deploying your own capital, though it adds legal complexity around SEC regulations and investor communications.

Final Thoughts From Rod Khleif

The BRRRR method is one of the most powerful wealth-building strategies in real estate — and in multifamily, the income-based valuation model makes it even more powerful than in single-family. Every dollar of NOI you create doesn’t just improve your cash flow. It multiplies into property value, which you can refinance against, which funds your next deal.

That’s the compounding engine that separates investors who own 10 units from investors who own 1,000.

The strategy requires discipline, patience, and rigorous underwriting. But for investors willing to do the work, it’s one of the fastest paths I know to building a portfolio that creates lifetime cash flow.

If you want to learn how to find, underwrite, and execute value-add multifamily deals — including BRRRR-style acquisitions — join me at my next Multifamily Bootcamp or grab your free copy of How to Create Lifetime Cash Flow Through Multifamily Properties.

Disclaimer: This article was written with the help of AI and reviewed by Rod and his team.