Capital Stacking Loan: How Smart Investors Structure Funding for Real Estate and Business

If you’re raising money for a large real estate acquisition or growing your business with outside capital, understanding the capital stack is non-negotiable. How you structure your funding affects risk, returns, and control. A strategy for stacking capital loans is essential.

In this article, I’ll explain what a capital stacking loan is, how it works in real estate and business lending, and how smart investors use this strategy to improve cash flow, optimize financing, reduce equity dilution, and find the best lenders for capital stacking loans.

What Is a Capital Stacking Loan?

A capital stacking loan is a financing strategy that combines different funding types. Each type has its own risk, return, and repayment terms. Together, they fund one project or deal.

This strategy is widely used in:

- Commercial real estate acquisitions

- Mergers and acquisitions

- Startup expansion

- Multifamily syndications

In real estate, capital stacking typically includes senior debt, mezzanine debt, preferred equity, and common equity. In a capital stacking business loan, layers may include term loans, lines of credit, convertible debt, and equity investment.

The goal? Build a financing structure that aligns investor and lender interests. Manage risk well. Maximize leverage while protecting your control and ownership.

How Does Capital Stacking Work?

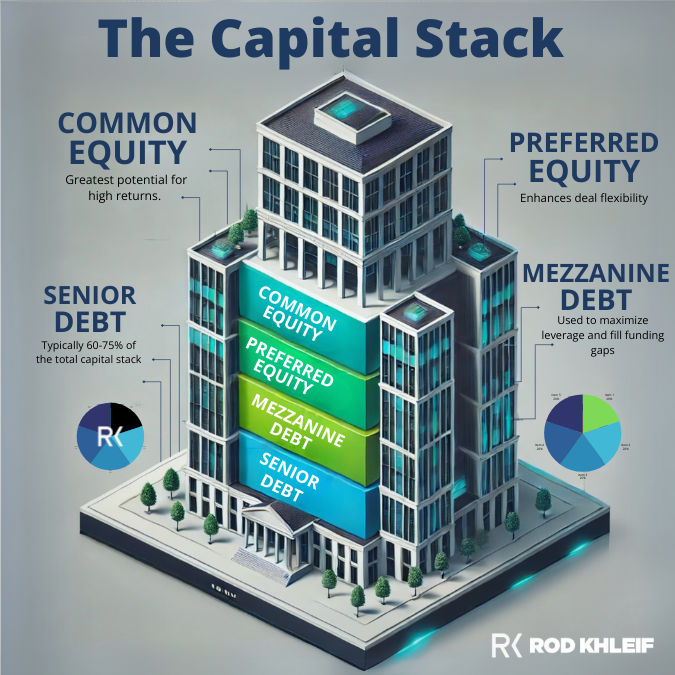

Think of the capital stack like a layered pyramid. Each layer has a different level of priority, risk, and potential return:

1. Senior Debt (Lowest Risk, Lowest Return)

This is typically a bank loan or mortgage secured by the asset. It gets repaid first and usually carries the lowest interest rate.

Key characteristics:

- First position lien on the property

- 65-75% loan-to-value (LTV) in real estate

- Lowest interest rates (often 5-8%)

- Most secure position in the stack

2. Mezzanine Debt (Moderate Risk/Return)

Subordinate to senior debt, this layer often comes from private lenders and carries higher interest rates. It may include equity kickers or profit participation.

Key characteristics:

- Second position behind senior debt

- 10-15% of total project value

- Higher interest rates (10-15%)

- May include warrants or equity upside

3. Preferred Equity (Higher Risk/Return)

Investors here receive fixed returns and priority over common equity holders but typically don’t have voting control.

Key characteristics:

- Preferred return (often 8-12%)

- Paid before common equity

- Limited or no voting rights

- Priority in liquidation scenarios

4. Common Equity (Highest Risk, Highest Return)

This includes the sponsor’s or business owner’s investment. Common equity gets paid last but also has unlimited upside potential.

Key characteristics:

- Last to be repaid

- Highest potential returns (15-25%+ IRR)

- Full voting control

- Bears the most risk

This structure lets the project owner or business operator control more of the asset with less personal capital. It still offers attractive returns to multiple stakeholders.

Want to learn more about the cap stack? Check out our comprehensive cap stack guide.

Benefits of Capital Stacking

1. Optimized Leverage Use more financing with less cash up front. This lets you scale faster. It also helps you keep cash for other opportunities.

2. Investor Alignment Give different classes of investors different roles, returns, and timelines based on their risk tolerance and investment objectives.

3. Risk Management Higher-risk investors take higher positions in the stack. This protects senior lenders. It also creates a buffer for the entire structure.

4. Flexible Terms Mix and match funding sources based on your specific needs, timeline, and market conditions.

5. Reduced Equity Dilution By using multiple debt layers, you can reduce the amount of equity you need to raise, maintaining more ownership and control.

Whether you’re funding a $10 million apartment complex or growing an e-commerce brand, capital stacking can be the key to efficient, scalable growth.

Capital Stacking in Real Estate: Practical Example

Let’s look at how a capital stack might work on a $10 million multifamily acquisition:

Total Property Value: $10,000,000

The Stack Breakdown:

- Senior Debt (70%): $7,000,000 bank loan at 6.5% interest

- Mezzanine Debt (10%): $1,000,000 at 12% interest with 2% equity kicker

- Preferred Equity (10%): $1,000,000 at 10% preferred return

- Common Equity (10%): $1,000,000 sponsor and investor equity

This structure lets the sponsor control a $10 million asset.They raise $2 million in total equity ($1M preferred + $1M common).The sponsor may contribute only $200,000 to $300,000 of their own capital.

Learn more about structuring multifamily syndications.

Capital Stacking Business Loan: Use Cases

Capital stacking isn’t just for real estate. Many growth-focused businesses use capital stacking loans to fuel expansion without over-relying on one financing type or diluting equity excessively.

Common business use cases:

Business Acquisitions Combine SBA loans, seller financing, and equity investment to acquire competitors or complementary businesses.

Startup Growth Use venture debt, angel capital, and lines of credit to scale operations while preserving founder ownership.

Franchise Rollout Blend term loans, equipment financing, and preferred equity to expand rapidly across multiple locations.

E-commerce Expansion Stack inventory financing, revenue-based financing, and equity to scale product lines and marketing.

This approach is especially useful for businesses seeking to avoid heavy equity dilution or retain majority ownership while still accessing large amounts of growth capital.

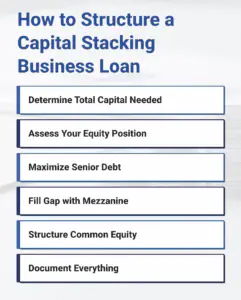

How to Structure a Capital Stacking Business Loan

Step 1: Determine Total Capital Needed Calculate exactly how much funding your project or business expansion requires, including contingencies.

Step 2: Assess Your Equity Position Decide how much you can or want to contribute personally and how much equity you’re willing to give up.

Step 3: Maximize Senior Debt Secure the largest senior debt position possible at favorable terms—this is your cheapest capital.

Step 4: Fill the Gap with Mezzanine or Preferred

Use mezzanine debt or preferred equity to bridge the gap.

This gap sits between senior debt and your equity contribution.

Step 5: Structure Common Equity Determine common equity requirements and structure profit splits, voting rights, and exit terms.

Step 6: Document Everything Work with experienced attorneys to create proper operating agreements, promissory notes, and security documents.

How to Find Capital Stacking Loan Lenders

Not all lenders understand or offer layered capital solutions. When seeking capital stacking loan lenders, look for:

1. Experience with Structured Finance Lenders who often work in commercial real estate, M&A, or venture lending. They understand complex capital structures.

2. Custom Deal Structuring Providers that can coordinate with other lenders or equity partners and aren’t rigid about “one-size-fits-all” terms.

3. Speed and Flexibility Especially important for bridge loans, mezzanine funding, or time-sensitive opportunities.

4. Track Record Lenders with proven experience in your specific asset class or industry.

Where to find them:

- Commercial banks with CRE divisions

- Private debt funds and family offices

- Mezzanine lenders specializing in real estate

- Business development companies (BDCs)

- Hard money lenders for short-term needs

- Capital advisory firms that can source multiple layers

You may need to work with multiple parties simultaneously, including banks, private lenders, equity investors, and specialized capital advisory firms.

Get our list of recommended multifamily lenders.

Common Capital Stacking Mistakes to Avoid

1. Misaligned Investor Expectations Clearly define returns, timelines, and exit strategies for each layer of the stack before accepting capital.

2. Overleveraging Just because you can stack more debt doesn’t mean you should. Maintain adequate cash flow coverage.

3. Ignoring Covenants and Restrictions Senior lenders often restrict additional debt. Read and understand all loan documents.

4. Poor Documentation Vague agreements lead to disputes. Use experienced attorneys to document every layer properly.

5. Underestimating Costs Each layer of capital has associated costs—origination fees, legal fees, and ongoing servicing costs.

Capital Stacking and Investor Returns

Understanding how the capital stack affects investor returns is crucial for both sponsors and investors.

Waterfall Distribution Example:

In a typical real estate syndication with a capital stack:

- Senior debt gets paid monthly interest and principal

- Mezzanine debt receives monthly or quarterly interest payments

- Preferred equity receives their preferred return (e.g., 8% annually)

- Common equity receives remaining cash flow and profit splits

Upon sale or refinance, the same priority applies. Common equity can still see strong upside if the property performs well.

Example return scenario on a successful deal:

- Senior Debt: 6.5% fixed return

- Mezzanine Debt: 12% + 2% equity participation = ~15% total return

- Preferred Equity: 10% preferred return

- Common Equity: Could see 20-30%+ IRR depending on deal performance

Learn how to analyze multifamily deals and investor returns.

Legal and Compliance Considerations

Capital stacking involves securities regulations, especially when raising equity from multiple investors.

Critical compliance requirements:

1. SEC Regulations Most private placements use Regulation D exemptions (Rule 506(b) or 506(c)). Work with securities attorneys.

2. Accredited Investor Verification If raising under 506(c), you must verify accredited investor status.

3. Private Placement Memorandums (PPM) Comprehensive offering documents that disclose all risks, terms, and deal structure.

4. Operating Agreements Define governance, voting rights, profit distributions, and exit provisions.

5. Subscription Agreements Legal contracts between the sponsor and each investor.

Never attempt to structure a capital stack without proper legal counsel. The costs of non-compliance far exceed legal fees.

Capital Stacking in 2026: Current Market Trends

Interest Rate Environment With the Federal Reserve’s recent rate decisions, senior debt costs remain elevated, making mezzanine and preferred equity more attractive for filling financing gaps.

Increased Institutional Interest More family offices and institutional investors are participating in mezzanine and preferred equity positions in well-structured deals.

Technology Platforms. New fintech platforms make it easier to find capital. They also help manage multiple layers of capital. This is especially helpful for smaller deals.

ESG Integration Lenders and investors increasingly favor projects with strong environmental, social, and governance components, potentially offering better terms.

Taking Action: Your Capital Stacking Strategy

Capital stacking is an advanced strategy that, if done right, unlocks powerful investment and business growth opportunities.

Whether you invest in real estate or run a business, understanding the capital stack helps you:

- Scale faster with less personal capital

- Protect your equity and maintain control

- Work effectively with sophisticated lenders and investors

- Structure deals that align everyone’s interests

Your next steps:

- Educate yourself on capital stack structures and terminology

- Build your team including attorneys, CPAs, and capital advisors

- Network with lenders who understand layered finance

- Start small and gain experience before tackling larger, more complex stacks

- Document everything meticulously from day one

If you’re evaluating a deal or building your first stack, don’t go it alone. Work with capital advisors, commercial lenders, or business finance experts to structure the most strategic stack possible.

FAQ: Capital Stacking Loan Strategy

Q: What exactly is a capital stacking loan?

A capital stacking loan is a structured financing method that combines multiple types of funding—like senior debt, mezzanine debt, and equity—to finance one deal. Each layer of the “stack” carries different risk, return, and repayment priority.

Q: Why is capital stacking used in real estate investing?

Capital stacking allows real estate investors to use more leverage, bring in different types of investors with varying risk tolerances, and reduce the amount of their own cash needed. It’s how you acquire large commercial deals while managing risk and return across multiple stakeholders.

Q: What’s the difference between senior debt and mezzanine debt?

Senior debt is your first lien mortgage with the lowest risk, lowest cost, and gets paid first. Mezzanine debt sits behind senior debt and is riskier, so it comes with higher interest rates and sometimes equity participation. Both are common in capital stacking real estate deals.

Q: How is capital stacking used in business loans?

In a capital stacking business loan, you might combine an SBA loan with seller financing, private equity, or a working capital line. The idea is to customize your financing so you don’t rely too heavily on any one source or give up too much ownership control.

Q: Is capital stacking only for big deals?

No. While it’s common in large commercial real estate or M&A transactions, smart investors and entrepreneurs use capital stacking principles for small business expansion, real estate flips, or mid-size multifamily deals. It’s about structure and strategy, not size.

Q: What’s preferred equity, and where does it fit?

Preferred equity sits between mezzanine debt and common equity. These investors receive a set return before common shareholders get paid, but they usually don’t have voting rights or operational control. It’s a popular middle ground in the capital stack.

Q: How do I find capital stacking loan lenders?

Look for lenders experienced in commercial real estate, M&A, or venture lending. These capital stacking loan lenders understand layered finance and can coordinate with other funding partners like private equity firms or family offices.

Q: Can I structure a capital stack myself?

You can, but I don’t recommend going solo on your first deal. Work with an experienced capital advisor or commercial lender who understands structured finance. It’ll save you time, stress, and potentially costly mistakes.

Q: What are the risks of capital stacking?

The more complex the stack, the more moving parts you’re managing. Misaligned incentives, repayment disputes, or changing interest rates can impact performance. That’s why clarity, proper contracts, and capable advisors are essential.

Q: How does capital stacking impact investor returns?

It can significantly improve returns for those higher in the stack, like common equity holders, but it also concentrates risk. A well-structured stack balances upside potential with downside protection, depending on each investor’s role and risk tolerance.

Q: Is capital stacking legal and SEC-compliant?

Absolutely, but if you’re raising money from multiple investors, especially in real estate syndications, you must stay SEC compliant. Work with syndication attorneys to ensure your private placement memorandums and offering documents are properly structured.

Q: What industries use capital stacking business loans?

Industries like commercial real estate, franchising, e-commerce, private equity rollups, SaaS companies, and tech startups commonly use capital stacking. Any business that needs growth capital but wants to manage dilution and risk can benefit.

Q: Where can I learn more about how syndicators structure capital stacks?

Download our Guide to Apartment Building Syndications or join our Multifamily Bootcamp. We walk through real-world examples of capital stacking, investor returns, and legal structuring, all with hands-on coaching.

Disclaimer: This post was written with the help of AI and edited by Rod and his team.

Join our next bootcamp!

Download our guide to apartment building syndications.