|

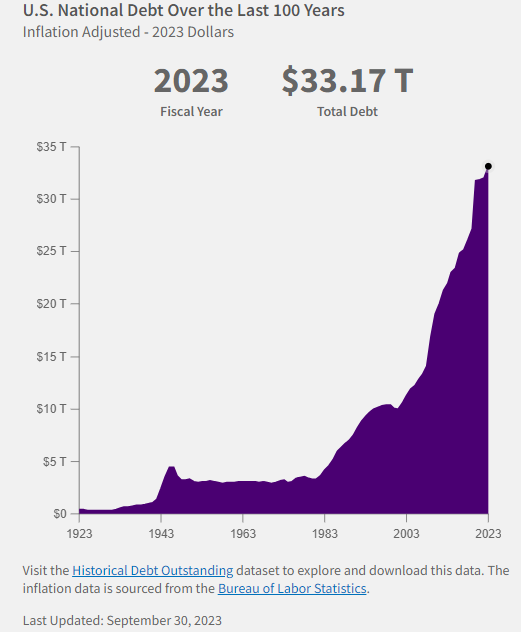

Bloomberg recently estimated that interest expense on the United States’ $33T debt just crossed $1T on an annualized basis. Federal receipts are $4.4T, which means almost a quarter of all revenue is consumed by interest. Interest expense has doubled over the past two years and will probably move higher with 2024 auction activity! “Rather go to bed without dinner than to rise in debt.” We certainly have come a long way from the frugal beginnings of the country. The chart below shows how rapidly and seemingly out of control the US debt has skyrocketed to around $100K for every person in the country. |

|

|

In 2024, 33% of our outstanding public debt matures ($7.6T) and must be reissued in a higher rate environment. On top of this $7.6T, the federal deficit could hit $2.0T in 2024, which means the Treasury would have to issue nearly $10T of new debt. The question is: where is this money going to come from and what impact will this have on interest rates and taxes? Of the $33T of debt, roughly 78% is owned by the public (70% US vs 30% International). The major US public owners include the FED ($6T, but they are no longer buyers), mutual funds, banks, states, pension funds and insurance companies. The international buying appetite has been falling over the past 10 years (dropping from 40% to the current 30%). The major international owners of US debt include Japan ($1.1T), China, UK, Belgium, Switzerland, Cayman Islands and smaller amounts from the rest of the world. After the recent weak treasury auction, US government officials warned that they are seeing waning demand from international buyers. China has been a net seller and Japan seems tapped out. The strong dollar is also working against the Treasury. The US dollar strength versus other currencies makes it attractive for international owners to sell US debt and use the dollars to buy their own currency, boosting the value. The remaining debt (22%) is owned by inter-government agencies including Social Security and Medicare. If you believe that Social Security and Medicare are bleeding off their surplus, then logically they will be net sellers over time as they use reserves to pay recipients. The auctions will come down to simple supply and demand. We know the supply is increasing and the demand is falling, which is bad for pricing. If the rates on Treasuries are attractive (higher) relative to other options, then we should be able to reissue the debt. In the most recent auction, the FED had to pivot to shorter term notes to entice buyers. Today, the 6-month treasury note yields 5.25% versus 4.0% for the 10-year, so clearly interest costs will increase in the short term if the US government is forced to issue short-term debt to attract buyers. If we don’t get our deficits under control, the situation will only grow worse. There is evidence, however, that higher interest rates on US debt are attracting new buyers. Two European money managers, Rathbones and Pictet, both recently announced an increase in their holdings of US Treasuries due to the attractive rates. Currently the US 10-year (4.0%) is higher than in the UK (3.8%), Spain (3.2%), Germany (2.2%) and Switzerland (0.8%), so it seems attractive relative to these options. We are not sure how this will all shake out, but at some point, something has to give because the trajectory we are on is unsustainable. At the end of the day, someone will have to pay for the sins of the past. Taxes need to move higher, and spending needs to be cut; both moves would hurt the economy. A weakening economy would have a ripple effect across all businesses and commercial real estate. We do not think the tax and financing benefits awarded to multi-family would be impacted during the “balance the budget phase” that is coming, due to the core nature of our product. However, the cloudy outlook reinforces our conservative thinking when evaluating deals. |