Multifamily Insurance: Coverage, Claims, and Risk Management

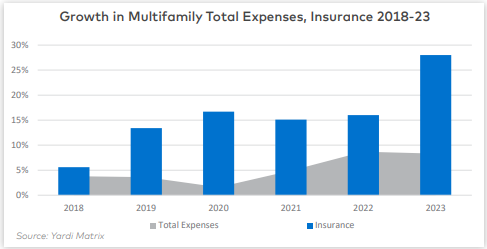

Proper insurance coverage for your multifamily property is both essential and costly. According to a recent Yardi report, multifamily insurance costs have risen 28% year over year. On average, insurance costs $636 per unit in the U.S., though rates in high-risk areas such as Miami ($1,405 per unit) and Houston ($1,115 per unit) are significantly higher. Since commercial real estate claims are often complex and subjective, understanding your policy is crucial to ensuring adequate protection in the event of a loss.

Risk Mitigation and Preventive Measures

Before facing an insurance claim, it’s vital to know your coverage details and implement proactive risk mitigation strategies. Regular property maintenance and thorough documentation can prevent costly issues. Keeping updated photos of your buildings and making simple fixes—like replacing rubber washing machine hoses every five years—can help prevent expensive disasters. Additionally, regular fire system inspections and awareness of slip-and-fall hazards can reduce liability risks. Implementing strong preventive maintenance policies can also lower insurance costs and minimize potential losses.

Key Components of Multifamily Insurance

Multifamily property insurance generally includes three main components:

- Comprehensive Coverage – Protects buildings and structures.

- Business Interruption Coverage – Compensates for lost income due to property damage.

- Liability Coverage – Protects against claims from injuries or damages on the property.

“The financial interests of insurance companies are best served by convincing policyholders to accept the lowest compensation possible.” — Forbes

Lessons from a Real-World Claim: Fire at Avalon Property

In April 2023, our Avalon property suffered a devastating fire that destroyed 20 units. This firsthand experience reinforced the importance of having both comprehensive and business interruption coverage. Immediately after the incident, we hired a public adjuster to guide the claims process and ensure that all losses were properly documented and justified.

Public adjusters bring expertise in pricing hidden costs—such as code compliance, engineering fees, and civil requirements—that many property owners might overlook. One critical lesson: Never begin rebuilding before finalizing the insurance settlement. Insurance companies frequently deny reimbursement for undocumented expenses, making it essential to agree on costs upfront.

To avoid disputes, our public adjuster compiled a 700-page estimate using the same software insurance companies use, ensuring every detail—from nails to structural components—was accounted for. This level of documentation left no room for negotiation, securing us a substantial settlement. Additionally, negotiating the timing of insurance payouts allowed us to receive a large portion of the funds early in the rebuilding process, keeping our project on track.

Business Interruption Coverage: The Hidden Challenge

Unlike comprehensive coverage, business interruption claims are highly subjective and often take longer to process. Insurers typically require proof of financial losses, which can delay payments. Most policies cover up to 12 months of lost income, but with longer permitting and construction timelines, this may no longer be sufficient. Consider extending coverage beyond a fixed period to avoid gaps in protection.

Another critical detail is ensuring that your policy covers “actual loss sustained” rather than a predetermined amount. This ensures that any revenue shortfall is fully accounted for.

If your property was undergoing renovations to increase rents, trailing financials may not reflect the actual financial impact of an event like a fire. In our case, our public adjuster assembled a forensic accounting team to reconstruct a pro forma P&L that factored in planned rent increases, seasonal leasing demand, and market trends. This strategy helped us secure a significantly higher settlement based on future earning potential rather than past performance.

Final Thoughts: Multifamily Insurance as a Critical Investment

Insurance is a fundamental part of multifamily investing. While you hope never to need it, if you own properties long enough, you will likely face a claim. Understanding what your policy covers, negotiating stronger terms, and taking preventive measures can make all the difference in securing your investment and minimizing financial risk.