If you want to protect and grow your wealth in today’s economy, you can’t just react—you need to anticipate.

The numbers coming out of Washington right now are clear: we’re heading into a decade defined by soaring deficits, rising interest costs, and persistent inflation. And while some investors are tightening up or pulling back, others are leaning in and strategically allocating capital to inflation-resistant assets like multifamily real estate.

Let’s break down what’s happening, what it means for your portfolio, and why real estate is one of the smartest hedges you can own right now.

The U.S. Deficit Is Getting Worse—Fast

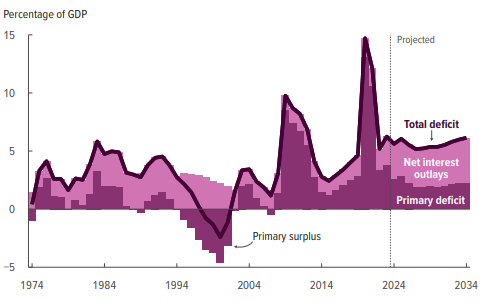

The Congressional Budget Office (CBO) is forecasting that annual federal deficits will grow from $1.6 trillion in 2024 to $2.6 trillion by 2034.

That’s not just a projection—it’s a warning. Even though tax revenues are expected to rise (from $4.4 trillion to $7.5 trillion), it still won’t come close to closing the gap. The federal government is spending far more than it’s bringing in, and that imbalance is growing.

Now, when deficits balloon, two things usually follow:

- Increased pressure on interest rates

- A higher risk of inflation

You can’t ignore either if you’re serious about investing.

Interest Payments on U.S. Debt Are Skyrocketing

Right now, the government is spending about $900 billion per year just on interest payments. By 2034, that number is expected to rise to $1.63 trillion.

That’s a 78% increase—and it doesn’t even factor in unexpected rate spikes or market resistance.

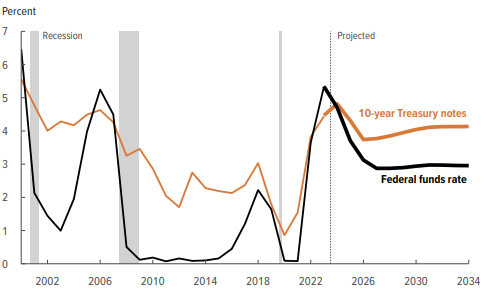

The CBO is projecting these costs based on modest assumptions: rates rising from 4.0% to 4.25%. But here’s the catch—what if demand for U.S. debt dries up?

If investors (domestic or international) start to walk away, the Treasury has two options:

- Raise rates further to make bonds more attractive (which would worsen the deficit), or

- Rely on the Federal Reserve to buy up debt, which would increase the money supply and, yes, inflation.

We’re already seeing early signs of this. The Treasury has reported weaker demand in recent auctions. That’s not just noise—it’s a flashing red light.

What Happens If the Fed Starts Printing Again?

If the Federal Reserve reverses course and starts buying bonds to ease the supply glut, it will effectively be injecting more money into the system.

And when the money supply increases faster than productivity?

You get inflation.

That means the dollars in your savings account, the yields from your bonds, and the returns from growth stocks all start losing purchasing power—fast.

And here’s the truth: even if the Fed manages inflation on paper, the cost of real goods—food, rent, gas, services—continues to rise. That’s where the squeeze hits.

Where Do You Invest When Inflation Won’t Go Away?

You don’t beat inflation with hope. You beat it with strategic allocation.

Historically, the best-performing asset classes during inflationary cycles include:

- Real estate (especially with fixed-rate debt)

- Commodities (like oil and gold)

- Consumer staples (companies that sell what people always need)

And the worst performers?

- Retail stocks

- Tech companies with high burn rates

- Durable goods (cars, electronics, etc.)

In short: inflation punishes anything that relies on cheap debt, low margins, or discretionary spending.

But it rewards real assets that generate predictable income and can adjust with rising prices.

Why Multifamily Real Estate Is Built for Inflation

Multifamily isn’t just another form of real estate—it’s one of the most reliable, durable, and inflation-resistant assets available.

Here’s why:

1. Fixed-Rate Debt = Locked-In Costs

When you buy a multifamily asset with long-term, fixed-rate financing, your interest expense stays the same—even as everything else rises. This creates a natural arbitrage between increasing income and fixed costs.

2. Rents Adjust With the Market

Unlike triple-net retail leases or long-term commercial contracts, multifamily rents can reset frequently—often every 12 months. That means as inflation pushes up wages and housing costs, your income can rise too.

3. Apartments Are a Core Need

In tough times, people may stop buying tech gadgets or upgrading their SUVs—but they won’t stop paying for a place to live.

That built-in demand makes apartments a defensive asset in volatile markets.

4. Value Appreciation Through NOI Growth

Inflation can lift gross income, and if you keep operating expenses in check, you grow your Net Operating Income (NOI). Since commercial properties are valued based on NOI, this leads directly to increased property value—and real wealth creation.

Your Next Move: Hedge the Right Way

I believe every investor should hold a diversified portfolio. But in this environment, it’s not just about diversification—it’s about intelligent allocation.

Cash and stocks alone won’t cut it. You need assets that grow with inflation, protect capital, and generate income.

Multifamily real estate—especially in growth markets and with solid operators—is one of the most strategic positions you can take right now.

Rod’s Final Thoughts

We’re heading into a future where debt is rising, inflation is sticky, and traditional strategies won’t be enough.

But there’s always opportunity—for those who are informed, prepared, and decisive.

Multifamily real estate has helped me and countless others not only preserve wealth—but multiply it. And it can do the same for you.

So here’s the question: Are you positioned for what’s coming next?

Because the decisions you make now could define your financial future for the next decade.

Let’s make them count.

— Rod