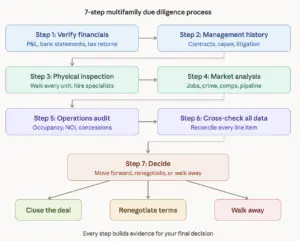

I use a 7 step due diligence process for every multifamily property I review. It has saved me from deal disasters that could have cost hundreds of thousands of dollars. Multifamily due diligence is the time between making an offer and closing, usually 30 to 60 days. During this time, you stop relying on the seller’s marketing package. You start verifying everything yourself. In my experience coaching over 2,000 students through their first multifamily acquisitions, I’ve found that the properties that look perfect in the glossy offering memorandum are often the ones hiding the biggest problems.

Most investors rush through due diligence because they’re excited about the deal. That’s exactly backward. The deal isn’t real until you’ve confirmed the numbers, walked the units, and stress-tested the assumptions.

Here’s the checklist my team and I use, and that our Warrior students have used to close on over 260,000 multifamily units collectively.

Why Due Diligence Decides Whether Your Deal Makes Money

Skipping or shortcutting due diligence is the fastest way to turn a promising investment into a money pit. A disciplined process helps you:

- Catch financial misrepresentation before you wire closing funds

- Quantify true repair costs so your renovation budget reflects reality, not hope

- Verify that rents are real . Not inflated by concessions, one-time payments, or phantom tenants

- Build negotiating leverage. Every issue you document is a reason to renegotiate price or terms

- Protect your investors if you’re syndicating. Your LPs are counting on your thoroughness

The cost of due diligence is a few thousand dollars in inspections and a few weeks of focused work. The cost of skipping it can be six or seven figures.

Due Diligence Step 1: Verify Every Financial Document Against Independent Sources

A seller’s proforma is a sales pitch. Your job is to find the gaps between their story and reality.

Request these documents on day one of your due diligence period:

- Operating statements for the last three years, including the current year-to-date

- Six months of bank statements. This is the single most important cross-reference because deposits don’t lie

- Utility bills for the last 24 months (all units plus common areas)

- Property tax bills for the last two years

- IRS tax returns and any related schedules for the last two years

- Utility deposit register

- Insurance policy with premium history and claims record

How to use them: Line up the operating statements against the bank deposits month by month. If the seller claims $50,000 in monthly rent collections but bank deposits average $42,000, you’ve found an $8,000/month problem. That’s $96,000/year in overstated income that directly inflates the property’s value at any cap rate.

I teach my students to build a reconciliation spreadsheet that maps every line item on the P&L to its source document. If a number can’t be verified, it doesn’t go into your underwriting model.

Run a Detailed Rent Roll Analysis

The rent roll is where most deals unravel. Request:

- Current rent roll with unit-by-unit detail and historical data going back two years

- Every lease agreement (the actual signed leases, not summaries)

- Security deposit register with amounts per unit

- Tenant payment history showing actual collections, not just charges

- Any concessions, move-in specials, or rent abatements currently in effect

Red flags that should slow you down:

- Turnover exceeding 50% annually, which signals management problems, property condition issues, or a market problem

- Rent amounts on leases that don’t match the rent roll or the operating statements

- A spike in occupancy or collections in the months just before listing. Sellers sometimes fill units with unqualified tenants to inflate numbers

- Delinquencies above 5-8% of gross potential rent

- Month-to-month leases on more than 20-30% of units. These tenants can leave at any time

Due Diligence Step 2: Investigate Property Management and Maintenance History

The property management operation tells you what you’re actually inheriting: not just a building, but a business with systems (or lack of systems) already in place.

Request and review:

- Current property management agreement, including fee structure and termination clauses

- Commission agreements with leasing agents and brokers

- All outstanding maintenance work orders (open and recently completed)

- Capital expenditure records for the past three to five years

- Any litigation history (lawsuits, code violations, tenant disputes) for the past five years

- Staff roster with roles, compensation, and tenure

What you’re looking for: A pattern of deferred maintenance is a signal that the seller has been extracting cash rather than maintaining the asset. If capital expenditures dropped to near zero in the last two years but the property is 20+ years old, you’re about to inherit a long list of repairs the seller didn’t make.

Check for repeat maintenance issues. If the same plumbing problem shows up in work orders every quarter, you’re looking at a system replacement, not a patch job.

If the current management company has high turnover, poor online reviews, or unresponsive communication during your due diligence period, factor in the cost and disruption of a management transition into your underwriting.

Due Diligence Step 3: Conduct a Hands-On Property Inspection

Photos and drone footage are marketing. Walking every unit is due diligence.

Before the inspection, gather:

- All service contracts: pool, trash, laundry, pest control, landscaping, elevator, security

- HVAC repair and replacement history

- Roof inspection reports and warranty documentation

- Insurance policy with claims history for the past three to five years

- Site plan, property survey, and any architectural or engineering plans

- Certificate of occupancy and all relevant permits

Walk Every Unit, Not Just a Sample

This is where I see investors cut corners most often. On a 100-unit property, inspecting 10 units and extrapolating is gambling with your capital. I’ve seen deals where the 10 “model” units were pristine and the other 90 needed $8,000+ each in renovations.

In every unit, document with photos and video:

- Flooring condition (carpet, tile, vinyl: what needs replacement vs. cleaning?)

- Kitchen: cabinet condition, countertops, appliances, plumbing under sinks

- Bathrooms: toilet, tub/shower, tile condition, water damage, mold

- HVAC system age and condition (check the manufacture date on the unit. If it is 15+ years old, budget for replacement)

- Electrical panel condition and capacity

- Windows and doors: seals, locks, screens, energy efficiency

- Water heater age and type

- Signs of pest infestation, water intrusion, or mold

Bring specialists for the big-ticket systems:

- Structural engineer for foundation, load-bearing walls, and any visible settling or cracking

- Roofing contractor for remaining useful life estimate

- Licensed plumber if the property has galvanized or polybutylene piping

- Electrician if the property has Federal Pacific or Zinsco panels (known fire hazards)

- Environmental consultant for Phase I ESA if required by your lender

Exterior inspection checklist:

- Parking lot and sidewalk condition (ADA compliance)

- Drainage and grading: does water flow away from buildings?

- Siding, stucco, or brick condition

- Stairwells, railings, and common area safety

- Laundry facilities and amenity spaces

- Signage condition and visibility from the road

- Dumpster areas, landscaping, and curb appeal

Due Diligence Step 4: Analyze the Local Market. A Good Building in a Bad Market Is Still a Bad Deal

Property condition is only half the equation. Market fundamentals determine whether your investment grows or stalls.

Research these factors before you close:

- Employment base: Who are the three to five largest employers within a 10-mile radius? Are they growing, stable, or at risk of layoffs or closure?

- Population trends: Is the metro area and submarket gaining or losing residents? Check census data and local economic development reports.

- Crime data: Pull neighborhood-level crime statistics, not just city averages. Walk the property at night.

- Rent comps: What are comparable properties charging per unit type? What concessions are they offering? Are rents trending up, flat, or declining?

- Occupancy comps: What’s the submarket vacancy rate? If it’s above 8-10%, there may be oversupply.

- New construction pipeline: Are new apartment developments planned or under construction nearby? New Class A supply can put downward pressure on older Class B/C rents.

- School quality: Even in workforce housing, school ratings affect tenant demand and retention.

- Infrastructure and amenities: Grocery stores, pharmacies, healthcare facilities, public transit access. These affect liveability and tenant quality.

- Regulatory environment: Check for rent control ordinances, eviction moratoriums, or proposed legislation that could affect operations.

Go beyond the spreadsheet. Visit the neighborhood at different times of day. Talk to local property managers. Eat at a nearby restaurant. Shop at the closest grocery store. You’ll learn more about the tenant experience in two hours of walking the area than in two days of reading reports.

Multifamily Due Diligence Step 5: Stress-Test the Property’s Operational Performance

Now step back from individual documents and look at the property as a business. Is this operation healthy, or is it being held together with Band-Aids?

Key questions to answer:

- What’s the difference between physical occupancy (units with tenants) and economic occupancy (units actually producing rent)? A property can be 95% physically occupied and 85% economically occupied if tenants aren’t paying.

- Has occupancy been stable, improving, or declining over three years? A downward trend during an otherwise strong rental market is a warning sign.

- What concessions is management offering? Free months, reduced deposits, gift cards. These are hidden costs that reduce effective rent.

- When were rents last increased, and by how much? A property where rents haven’t been raised in three years may have upside, or it may have tenants who will leave when you raise them.

- Are maintenance expenses suspiciously low? Below-market maintenance spending usually means deferred repairs you’ll pay for later.

- What’s the trend in Net Operating Income? If NOI has been flat or declining while the market has been growing, there’s an operational problem.

- What’s the payroll-to-revenue ratio? Overstaffing or understaffing both create problems.

Run your own underwriting model using the verified numbers from Steps 1-4, not the seller’s proforma. Your model should include realistic assumptions for rent growth, expense inflation, vacancy, capital expenditures, and debt service. If the deal doesn’t work with conservative assumptions, it doesn’t work.

Due Diligence Step 6: Cross-Check Everything and Build Your Reconciliation

This is where you put all the pieces together. Before you make your final decision, every number in your underwriting should trace back to a verified source document.

Reconciliation steps:

- Compare the P&L line by line against bank deposits and tax returns. Do the revenue numbers match across all three sources?

- Verify that each lease in the lease file matches the corresponding line on the rent roll

- Confirm that actual tax bills match the property tax line item in the operating statements (sellers sometimes use lower “projected” numbers)

- Check that insurance costs reflect current coverage, not an expired policy at a lower rate

- Compare utility costs against the utility bills you collected. Are there units where the owner pays utilities that are not reflected in expenses?

- Benchmark every expense category against industry standards for the property’s age, class, and market. If the seller shows $800/unit/year in maintenance on a 1975 property, that’s almost certainly understated.

Document every discrepancy. Each one becomes a data point for renegotiation in Step 7.

Due Diligence Step 7: Renegotiate, Restructure, or Walk Away

Due diligence isn’t just about confirming a deal. It is about deciding whether the deal still makes sense given what you’ve learned.

After completing your analysis, you have three options:

Move forward if the property meets or exceeds your underwriting assumptions and the risk profile aligns with your investment criteria.

Renegotiate if due diligence revealed issues that change the economics. Common renegotiation points include:

- Purchase price reduction based on actual NOI vs. stated NOI

- Seller credits for deferred maintenance or capital expenditures

- Extended closing timeline to allow for additional inspections or financing adjustments

- Holdback escrow for known repair items

- Seller-financed portion to bridge a gap between appraised value and contract price

Walk away if the property has fundamental problems that can’t be solved with a price reduction: environmental contamination, structural failure, market decline, or a seller unwilling to negotiate in good faith.

Walking away is not failure. It’s discipline. The best investors I’ve worked with pass on more deals than they close because they have standards they won’t compromise. In the Warrior program, we review deals together specifically to build this muscle. Knowing when to say no is as valuable as knowing how to underwrite.

Want a Printable Version of The Due Diligence Checklist?

Download the complete Multifamily Due Diligence Checklist as a PDF, the same document our Warrior students use when evaluating deals.

[Download the Free Due Diligence Checklist →]

Ready to Put This Into Practice on Real Deals?

Due diligence is where theory meets reality. If you’re ready to evaluate your first multifamily deal, or want expert eyes on a deal you are already working on, Rod’s team can help.

Our Warrior students get live deal review calls where we walk through due diligence findings together, catch issues before they become expensive, and help you negotiate from a position of strength.

Apply to the Warrior Program →

Frequently Asked Questions About Multifamily Due Diligence

How long does the due diligence period typically last for a multifamily property?

Most multifamily purchase agreements include a due diligence period of 30 to 60 days, though larger or more complex deals may negotiate 60 to 90 days. The clock starts when the purchase and sale agreement is executed. Plan your inspection schedule, document requests, and specialist appointments for the first week so you use every day productively. If you reach the end of your period and haven’t finished, you may be able to negotiate an extension, but you’ll have more leverage if you started strong and can show specific outstanding items rather than asking for more time because you procrastinated.

How much does due diligence cost for a multifamily acquisition?

For a typical 50 to 150 unit property, expect to spend $10,000 to $30,000 on third-party reports and inspections. This typically includes a property condition assessment ($3,000 to $8,000), Phase I environmental site assessment ($2,000 to $5,000), appraisal ($3,000 to $7,000), survey ($2,000 to $5,000), and title search and insurance ($2,000 to $5,000). Smaller properties cost less, and larger or more complex assets cost more. This investment is a fraction of the purchase price and can save you from six-figure mistakes. Most of these costs are non-refundable if you walk away, which is why you should front-load your financial analysis. Kill the deal on paper before spending on inspections.

What are the biggest red flags during multifamily due diligence?

The issues that kill deals most often are financial misrepresentation (income overstated or expenses understated), significant deferred maintenance that wasn’t disclosed, environmental contamination requiring remediation, title issues or unrecorded liens, and market fundamentals that don’t support the seller’s rent projections. In my experience, the most common problem is a gap between what the seller’s operating statements claim and what the bank deposits actually show. If the numbers don’t reconcile, everything else becomes suspect.

Should I inspect every unit or just a sample?

Inspect every unit. Sampling introduces risk that you’ll miss the worst units, and sellers know which units they’d prefer you not see. On a large property where full inspection isn’t practical within the timeframe, inspect a minimum of 20 to 25 percent of units plus every vacant unit, every unit with outstanding maintenance requests, and every unit the seller seems reluctant to show you. Budget the time and cost to do this right. It is the best insurance you’ll buy on the deal.

What’s the difference between a property condition assessment and a regular home inspection?

A property condition assessment is a commercial-grade evaluation conducted by a licensed engineering firm, not a residential home inspector. A PCA covers structural systems, mechanical systems, electrical, plumbing, building envelope, site work, ADA compliance, and provides a replacement reserve schedule estimating future capital expenditure needs. Most commercial lenders require a PCA. A residential-style home inspection is typically insufficient for multifamily properties above four units because it doesn’t assess building systems at a commercial scale or project future capital needs.

Can I back out of a deal after due diligence if I find problems?

Yes, if you’re still within your contractual due diligence or feasibility period, you can terminate the agreement, usually with the return of your earnest money deposit, minus any non-refundable “hard” earnest money or independent consideration outlined in the contract. Once the due diligence period expires, your earnest money typically goes “hard,” meaning you forfeit it if you back out. This is why it is critical to complete your analysis before the deadline and make your go or no-go decision with time to spare.

What documents should I request on day one of due diligence?

Send your complete document request list to the seller or broker within 24 hours of executing the purchase agreement. At minimum, request three years of operating statements, 12 months of bank statements, current rent roll with all leases, utility bills for 24 months, tax returns, property tax bills, insurance policy with claims history, all service contracts, management agreement, capital expenditure records, litigation history, and any environmental reports. The faster you receive these documents, the more time you have to analyze them. Slow document delivery from a seller is itself a red flag.

Rod Khleif is a multifamily real estate investor, educator, and host of the Lifetime Cash Flow Through Real Estate Investing podcast, with over 20 million downloads. He has personally owned and managed over 2,000 properties and his students have collectively acquired over 260,000 multifamily units through the Warrior program.